Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

BankAmericard® Credit Card Review 2025: 0% APR Relief – Is It Worth It?

February 6, 2025

.webp)

A low-interest credit card with a true 0% intro APR for 18 months can be a lifesaver for tackling debt – but does the BankAmericard® deliver enough value despite offering no rewards?

Key Features of the BankAmericard Credit Card

The BankAmericard® Credit Card is designed for one primary purpose: helping you pay off debt or finance a large purchase without interest. Here are its headline features:

- 0% Intro APR for 18 billing cycles on new purchases and balance transfers. This is one of the longest 0% APR periods available on any credit card.

- No annual fee – it costs nothing to carry this card.

- Balance transfer fee: 3% of the amount (minimum $10) for transfers in the first 60 days, then 4% thereafter. Like most 0% cards, a small upfront fee applies to moved debt.

- Regular APR after intro: ~15.24% – 25.24% Variable. No penalty APR – meaning if you pay late, your interest rate won’t jump as a punishmen.

- No rewards program: This card does not earn cash back or points on purchases. Its value is purely in interest savings.

- Credit level needed: Generally good to excellent credit is required. It’s not aimed at people with new or poor credit.

In short, the BankAmericard is a simple, no-frills card. It’s all about that long 0% APR period. If you have high-interest debt or an upcoming expense you need to spread out, this card offers breathing room.

[[ SINGLE_CARD * {"id": "194", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "People With Good Credit Score", "headerHint": "No-Frills Card"} ]]

Pros & Cons

Pros:

- Lengthy 0% APR period – 18 months with no interest on purchases and balance transfers is among the longest on the market. This can save you a ton in interest. For example, carrying a $10,000 balance on a typical 20% APR card would accrue about $3,960 in interest over 18 months – the BankAmericard can potentially save you that money by giving you a window to pay down principal interest-free.

- No annual fee – There’s no cost to hold the card, so you can focus on paying your balance down, not paying a fee.

- No penalty APR – Unlike many cards, a late payment won’t jack up your interest rate. That’s forgiving if you slip up.

- Simple, easy to understand – No complicated rewards or bonus categories. It does one thing and does it well: provides a temporary interest-free loan.

Cons:

- No rewards or cashback – If you’re debt-free and looking for rewards on spending, this isn’t the card for you. It earns 0% back on everything.

- No sign-up bonus – Many cards entice with a cash or points bonus; BankAmericard’s “bonus” is essentially the intro APR offer. There’s no immediate reward for getting the card, aside from potential interest savings.

- Balance transfer fee – You’ll pay 3% of any balance you move onto the card (within 60 days). This is fairly standard (and lower than some cards that charge 5%), but it’s a cost to calculate.

- High ongoing APR – Once the 18 months are over, the interest rate could be around 15-25% depending on your credit. That’s normal for a credit card, but it means you don’t want to carry a balance after the intro period ends (or it gets expensive again).

- Good credit required – This card isn’t easy to get if your credit score isn’t in the “good” range or above. Bank of America typically looks for ~670+ FICO. If you’re still building credit or have some dings, you might not qualify.

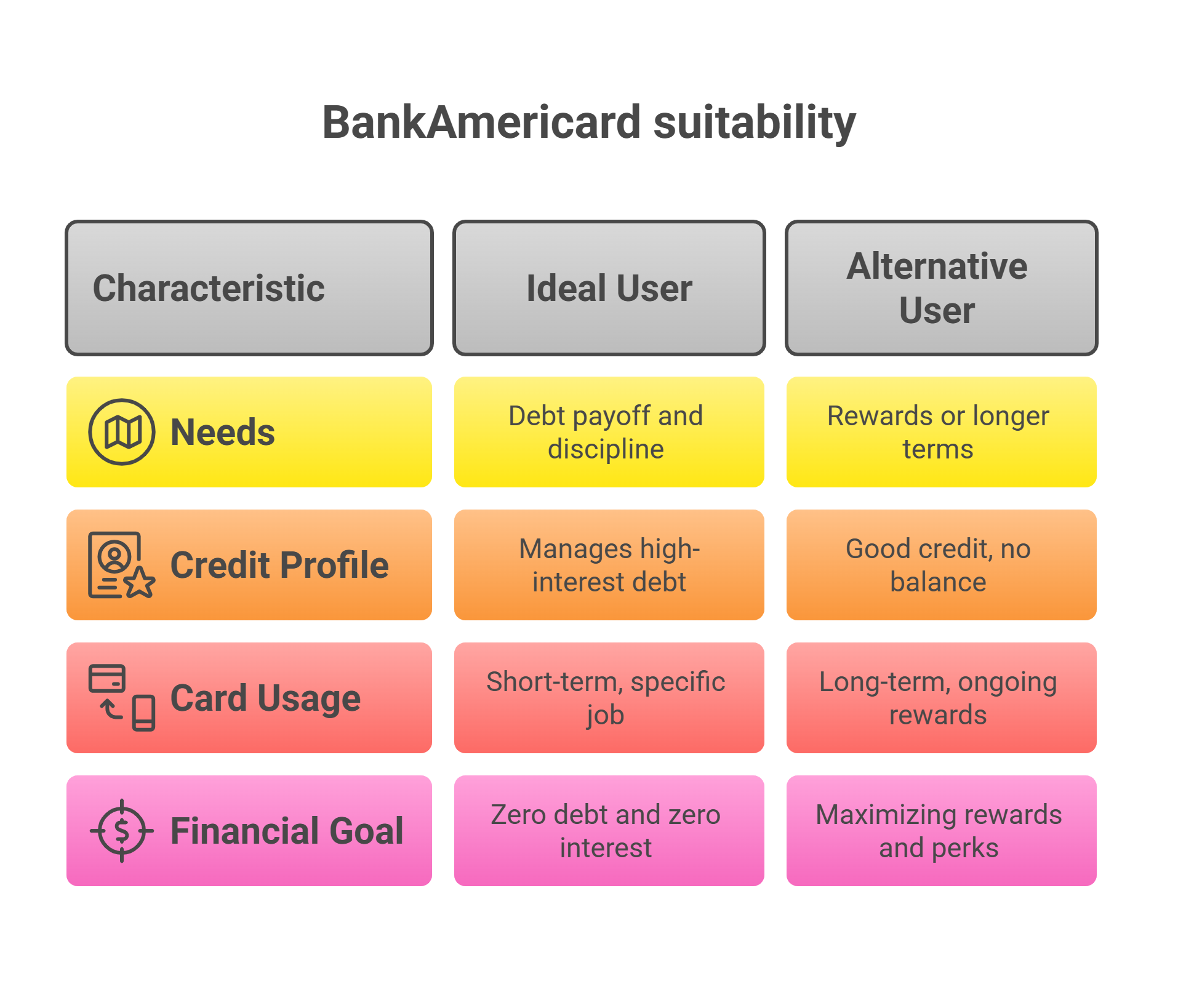

Who Should Consider the BankAmericard?

Ideal for: Individuals looking to eliminate existing credit card debt or finance a one-time big expense with zero interest. If you have a chunk of high-interest credit card debt, moving it to BankAmericard can give you 18 months of breathing room.

Not ideal for: Everyday spenders or rewards seekers. If you pay your balances in full and want rewards, plenty of other cards offer cash back, points, or miles. The BankAmericard literally gives you nothing in rewards – its value is only in not charging interest. Also, if you’re someone with less-than-good credit or no credit history, this card may be out of reach for now.

Alternatives to consider: If you want a long 0% APR but also some rewards or a lower credit requirement:

- Look at other balance transfer cards: For instance, Citi Simplicity® offers 21 months 0% on balance transfers, though its 0% on new purchases lasts only 12 months. Citi Simplicity also charges no late fees – a factor if you worry about missing payments.

- Wells Fargo Reflect® Card is another card with up to 21 months 0% APR. It’s great if you need the absolute longest runway to pay off debt. No rewards on that one either, though.

[[ SINGLE_CARD * {"id": "3351", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Those Seeking Simplicity", "headerHint": "No Annual Fee"} ]]

- If your credit is not quite good/excellent, you might try a card like Discover it Cash Back Credit Card or Chase Freedom Unlimited®. These have slightly shorter 0% intro periods (15 months), but are a bit easier to get approved for and do offer rewards.

[[ SINGLE_CARD * {"id": "821", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Cash Back Seekers", "headerHint": "Rotating Categories"} ]]

[[ SINGLE_CARD * {"id": "497", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Cash Back Seekers", "headerHint": "Fantastic Cash Back Card"} ]]

In summary, BankAmericard is best for someone solely focused on cutting interest costs and who needs as long a break from interest as possible. If that’s you, it can be a powerful tool. If you have other goals (rewards, travel points) or only need a shorter-term promo, another card might offer more overall value.

Comparing BankAmericard® Credit Card with Other Credit Cards

When considering the BankAmericard® Credit Card, it's helpful to compare it with other popular options in the credit builder card category:

Chime Credit Builder Secured Visa® Credit Card:

- Annual fee: $0

- Security deposit: Flexible, based on the amount transferred to Credit Builder account

- Key features: No credit check to apply, reports to all three major credit bureaus

- Standout feature: No minimum security deposit required

Capital One Quicksilver Secured Cash Rewards Credit Card:

- Annual fee: $0

- Security deposit: Minimum $200, which becomes your credit limit

- Key features: 1.5% cash back on most purchases, automatic credit line reviews

- Standout feature: Earn rewards while building credit

Current Build Visa® Credit Card:

- Annual fee: $0

- Security deposit: Flexible, based on the amount transferred to Build account

- Key features: No credit check required, reports to all three major credit bureaus

- Standout feature: Linked to Current banking app for easy fund transfers

Each card offers unique benefits tailored to different spending habits and preferences. Consider your personal financial goals when choosing the best card for you.

Key Takeaways:

- BankAmericard® Credit Card excels in helping people pay off debt

- Chime Credit Builder offers flexibility with no minimum deposit

- Capital One Quicksilver Secured provides cash back rewards

- Current Build integrates with banking app for convenient use

[[ CARD_LIST * {"ids": ["3069","3058", "5132"]} ]]

How to Use the 0% APR Period Wisely

Getting 18 months of 0% APR is a golden opportunity – but you’ll want to have a plan to make the most of it:

- Transfer or charge right away: The clock starts when you open the card. If you have a balance to transfer, do it in the first 60 days to lock in the 0% rate on that balance and get the lower 3% fee. If you wait longer, you’ll pay the higher 4% fee and miss out on some interest-free months.

- Divide your debt by 18 (months): Aim to pay roughly 1/18th of your balance each month (about 5.5%). For example, $9,000 of debt could be ~$500 a month. This ensures you pay it off before interest kicks in. At the very least, mark your calendar for 18 months from now with the expected end date of the promo.

- Avoid new purchases after the promo if you can’t pay in full: Once the 0% period ends, any remaining balance or new purchase will start accruing interest at ~15-25% APR. You don’t want to slide back into paying interest after all that. So, try to clear the balance, and consider not using this card for new spending beyond what you planned, unless you can pay those off each month.

- Don’t miss payments: The 0% APR deal stays intact even if you’re late (no rate hike), but a late payment can still hurt you. You’ll incur up to a ~$40 fee and could ding your credit score, which isn’t worth it. Set up autopay for at least the minimum due to be safe.

By sticking to a plan, you can emerge at the end of 18 months debt-free without paying a dime in interest. That’s the whole point of this card!

Kudos Tip: Maximize Your Card Strategy with Kudos

Before applying for a specialized card like BankAmericard, consider how it fits into your overall credit card strategy. This is where Kudos, your AI-powered credit card companion, can help:

- See All Your Cards in One Place: Kudos lets you connect and monitor multiple credit cards. If you add BankAmericard to your wallet, Kudos will help ensure you’re using it at the right times – and not using it when a better reward card is an option.

- Personalized Card Recommendations: If you’re not sure the BankAmericard is your best option, Kudos can analyze your profile and suggest alternatives. Our goal is to make sure you have the right card for your needs – debt payoff or otherwise.

- Never Miss a Deadline: Kudos can send you smart reminders. For instance, we’ll notify you before your 0% intro period ends, so you can plan your next move. Avoiding surprise interest is a key part of saving money!

Currently, Kudos is offering $20 back after your first eligible purchase — just sign up for free with code "GET20" and let Kudos help you maximize your credit cards. Put your cards to work, and save money while you’re at it!

Bottom Line: Should You Get the BankAmericard?

The bottom line is that the BankAmericard® Credit Card can be a valuable tool for the right person. If you’re staring at a pile of high-interest debt or planning a big expense that you want to pay off over time, this card offers a lengthy reprieve from interest charges. In that sense, it can save you money and help you get ahead financially instead of drowning in ~20% APR fees.

However, if you’re someone with good credit who never carries a balance, a different card will likely serve you better (why forego rewards if you’re not utilizing the 0% perk?). Similarly, for those who do need a balance transfer card but can qualify for others, consider the alternatives – maybe you want the absolute longest term (21 months), or you prefer a card with some rewards once you’re done paying off the balance.

Our advice: evaluate your needs. The BankAmericard is excellent for debt payoff and discipline, but it’s not a card you keep using forever – it has a specific job. If you take it on, have a plan to become debt-free by the end of the intro period. And remember, you don’t have to navigate this alone – tools like Kudos can assist in optimizing your credit card usage alongside BankAmericard, ensuring you maximize rewards on other cards and never miss a beat on your debt payoff plan.

In 18 months, you could be celebrating zero debt and zero interest paid – that’s the real reward of the BankAmericard®. If that’s the goal you need to hit, this card is absolutely worth a look. Just go in with eyes open, a payoff strategy in hand, and let Kudos help you along the way. Here’s to being debt-free (and smart about it)!

FAQ – BankAmericard Credit Card

What credit score do I need for the BankAmericard Credit Card?

You’ll typically need good to excellent credit for approval. That usually means a FICO score around 670 or higher. In fact, many successful applicants report scores in the 700s. If your score is lower, BankAmericard may be hard to get – consider improving your credit first or looking at cards for fair credit.

Does the BankAmericard® credit card offer rewards?

No – the BankAmericard does not offer any ongoing rewards or cash back. Its benefit is the 0% intro APR period. If earning points or cash back is important to you, you’ll want a different card for your everyday spending (and you can use Kudos to find one that matches your needs).

Is there a balance transfer fee?

Yes. For any balances you transfer to BankAmericard, there’s a 3% fee (min $10) during the first 60 days of opening the account. After that window, any new balance transfers cost 4%. There’s no fee to transfer from BankAmericard to another card, but you’d pay that other card’s fee instead if you do a future transfer.

Is the BankAmericard a Visa or a Mastercard?

The BankAmericard® credit card is actually a Mastercard, not a Visa. This doesn’t make much difference in acceptance – Mastercard is widely accepted worldwide wherever Visa is. It just means it runs on the Mastercard network and comes with Mastercard’s standard benefits (like zero liability protection, etc.).

Can students apply for the BankAmericard (is there a student version)?

Bank of America offers a BankAmericard® Credit Card for Students, which has the same 0% APR deal. However, it’s a bit of an oddball – it still requires a good credit score in practice. Many students may not qualify if they have limited credit history. Unless you’re an authorized user on someone else’s card or have built credit already, it might be tough to get. Students who are just starting out might be better off with a beginner student credit card (perhaps one that earns some cash back). After you build credit, you could then consider something like BankAmericard for a big purchase or debt payoff during senior year or after graduation.

What happens after the 18-month 0% APR period ends?

Any remaining balance will start to accrue interest at the regular APR (around 15.24%–25.24% variable) based on your credit. For example, if you still have $2,000 left unpaid, interest will start adding up on that amount each day. Before you reach month 19, you should ideally have a $0 balance on the card. If you can’t pay it all off, one strategy is to look for a new balance transfer offer at that time (though balance transfer “hopping” has limits and fees). Kudos can help you track when your promo period ends so you’re not caught off guard.

Is the BankAmericard worth it if I don’t have any debt right now?

Probably not. If you don’t need to carry a balance or avoid interest, then the main benefit of BankAmericard is moot. You’d be better served with a rewards card to earn cash back or miles on your purchases. BankAmericard is worth it in specific scenarios – mainly when you actively need the 0% APR. It’s a niche, purpose-driven card.

Supercharge Your Credit Cards

Experience smarter spending with Kudos and unlock more from your credit cards. Earn $20.00 when you sign up for Kudos with "GET20" and make an eligible Kudos Boost purchase.

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.