Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Emergency Fund 101: What It Is and How to Build One

July 1, 2025

An emergency fund is a sum of money set aside to cover life’s unexpected surprises – the unplanned expenses that pop up without warning. Think of sudden events like a surprise medical bill, car breakdown, or losing your job. An emergency fund is your financial safety net to handle those situations without derailing your life or racking up high-interest debt. In this guide, we’ll cover what an emergency fund is, why it’s so important, and how you can build one from scratch, even on a tight budget. By the end, you’ll have a clear plan to create your own personal safety net for life’s “uh-oh” moments.

Why Do You Need an Emergency Fund?

Life is full of surprises – some fun, and some expensive. An emergency fund ensures that an unexpected bill doesn’t become a financial crisis. Here are a few reasons why having an emergency fund is essential:

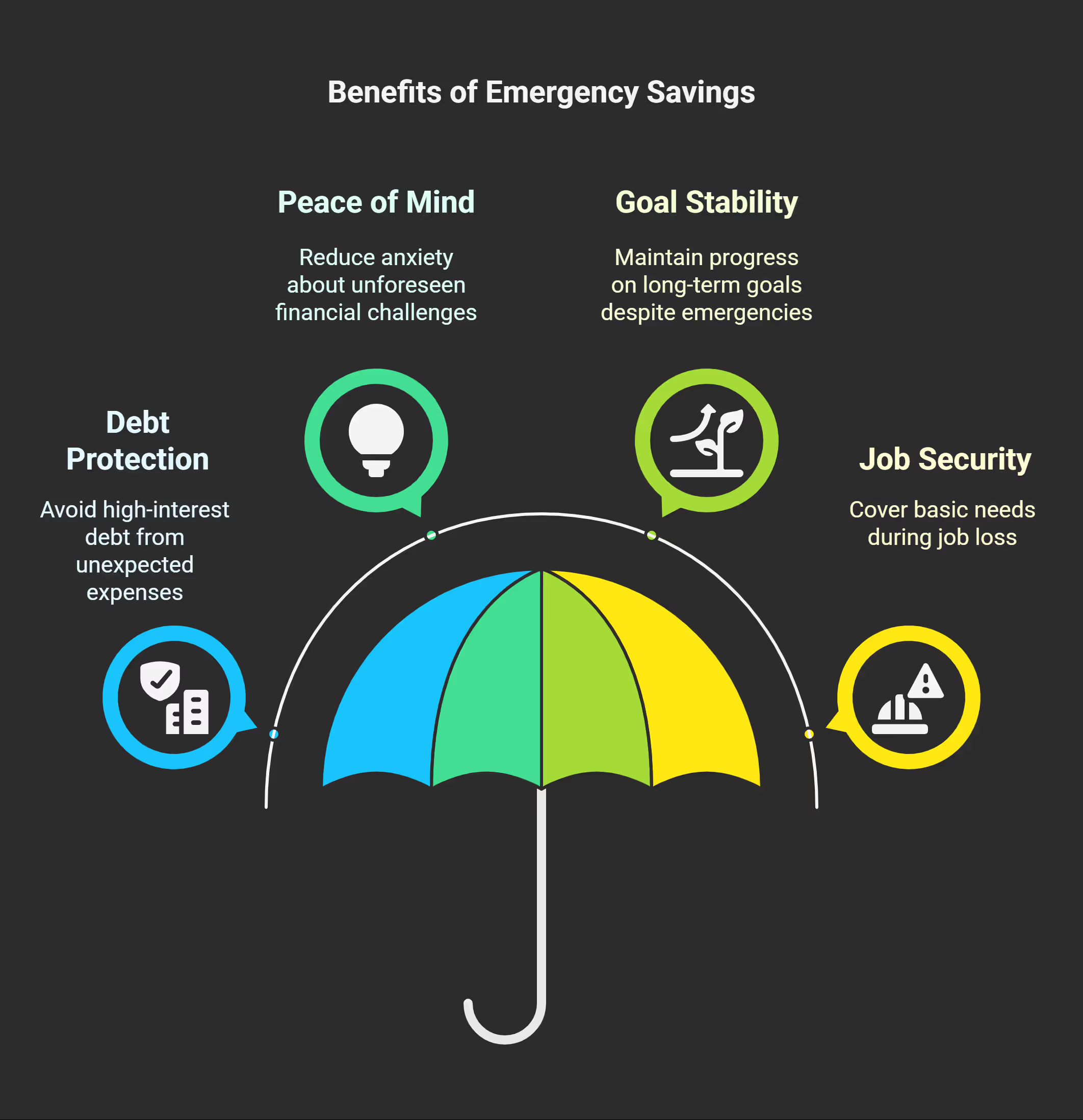

- Protect Yourself from Debt: Without savings, a surprise $1,000 expense might push you to swipe a credit card or take a loan. An emergency fund helps you avoid high-interest credit card debt or payday loans. It’s much cheaper (and less stressful) to pay from savings than to owe money later with interest.

- Peace of Mind: Knowing you have a cushion gives you peace of mind. It reduces anxiety about the “what-ifs.” You can sleep better knowing a car repair or leaky roof won’t force you to choose between bills.

- Stay on Track with Goals: With a safety net, an emergency won’t force you to pause long-term goals like buying a home or investing for retirement. Your savings insulates your life plans from short-term shocks.

- Job Security (or Insecurity): If you unexpectedly lose your job, emergency savings can cover your basic needs while you search for a new position. This is especially crucial if you don’t have other support.

In short, an emergency fund is your financial first-aid kit. You hope you won’t need it often, but it’s critical to have it ready. It’s not a luxury – it’s a necessity for everyone, no matter your income.

What Exactly Counts as an “Emergency”?

Not every unexpected cost is an “emergency” that merits dipping into this fund. Generally, true emergencies are necessary, urgent, and unexpected expenses. For example:

- Emergencies: Job loss, medical emergencies or big urgent dental work, major car repairs after an accident, necessary home repairs (like a furnace dying in winter), emergency travel for a family crisis.

- Not Emergencies: Things like a tempting vacation deal, holiday gifts, or a sale on a new phone – those might be unexpected wants, but not needs. Even routine irregular expenses (annual car insurance, maintenance, etc.) aren’t emergencies; you can anticipate them (often these are what we call “rainy day” expenses – more on that later).

A good rule of thumb: If the expense is something that affects your health, safety, or basic livelihood and you must pay it soon, it’s likely an emergency. Part of building your fund is also learning to only use it for true emergencies. This discipline ensures the money is there when you really need it.

How Much Should You Save in Your Emergency Fund?

You might have heard the classic advice: save 3 to 6 months’ worth of living expenses in an emergency fund. This is a common recommendation from financial experts and bankschase.com. In practice, the right amount can vary (we cover this in detail in our dedicated article on [how much you need in an emergency fund]).

Here’s a brief overview:

- Start with a Starter Fund: If you’re new to saving, aim for a starter emergency fund of about $500 to $1,000. This amount handles many small crises (a surprise car fix, a minor medical bill). It’s an achievable goal to get you going. In fact, one survey suggests setting aside $500 is a great first milestone.

- Build to 3 Months of Expenses: Once you have the starter fund, keep going. Try to accumulate enough to cover 3 months of your essential expenses. “Essential” means rent/mortgage, utilities, groceries, insurance, minimum debt payments – the stuff you must pay to get by each month.

- Aim for 6+ Months if Possible: If you can, having 6 months of expenses saved is a robust cushion. This is especially important if you have a less stable income, dependents, or own a home (bigger emergencies possible). During events like a global pandemic or recession, 6 months or more of savings proved incredibly valuable.

Example: Let’s say your bare-bones monthly needs total $2,500. A three-month fund is $7,500. A six-month fund is $15,000. That might sound high, but remember – you don’t have to save it all overnight. You’ll build it gradually (next section shows how).

Can you save more than 6 months? Sure, some people feel more secure with 9-12 months saved, and that’s okay. Just make sure it doesn’t cause you to neglect other goals (like investing for retirement). There’s also an opportunity cost to holding a very large amount of cash (inflation can erode its value), so many experts say 6 months is a sweet spot for most. (If you ever end up with an extra large cash pile, you might invest the excess – but that’s a good “problem” to discuss with a financial advisor.)

How to Build an Emergency Fund (Step by Step)

Building an emergency fund might feel daunting, but it’s absolutely doable with small consistent steps. Here’s how to get started:

1. Set a Clear Savings Goal:

First, determine your target. Is it $1,000? Three months of expenses? Having a number gives you something to work toward. (If you calculated you need, say, $9,000 for three months of expenses, that’s your goal. But you’ll achieve milestones along the way, like $1k, $3k, etc.)

2. Make a Budget and Find Room to Save:

Look at your monthly income and expenses (yes, the “B” word – budget!). Identify a realistic amount you can save each month. Treat your emergency fund contribution like a bill to yourself. For example, decide “I will pay $100 into my emergency fund every payday.” You may need to trim some optional spending (streaming services, dining out) to free up that cash – even $50 a month adds up.

3. Automate Your Savings:

This is key. Set up an automatic transfer from your checking to a dedicated savings account every month or paycheck. Automating makes saving painless and consistent – you won’t forget or be tempted to skip it. Many people succeed by “paying themselves first” this way.

4. Save Windfalls and Extras:

Whenever you get unexpected money – a bonus, tax refund, stimulus check, birthday gift money – put a chunk of it (or all of it) into your emergency fund. These infusions can boost your fund fast. For instance, a $600 tax refund could instantly double a $600 fund to $1,200.

5. Keep the Funds Accessible but Separate:

Put your emergency savings in a separate savings account (ideally a high-yield account – more on that in a bit). Keeping it separate from your everyday checking prevents accidental spending. But ensure it’s still easily accessible (liquid) so you can withdraw in an emergency without hassle.

6. Use Budgeting Hacks:

Try budgeting methods like the 50/30/20 rule (50% needs/30% wants/20% savings) and include your emergency fund in that 20% for savings/debt. If 20% is too high right now, even 5-10% of your income directed to savings will build the fund. Increase the contributions when you can (say you pay off a debt – redirect that payment amount into savings).

7. Monitor and Adjust:

Check your progress each month. It can be motivating to watch your fund grow. If you get a raise or eliminate an expense, bump up your saving rate. On the flip side, if money’s tight one month, it’s okay to contribute a bit less – just resume next month. Consistency over time is what matters.

By following these steps, you’ll gradually accumulate that safety net. It might take months or a couple of years to reach your ultimate goal, but even a small fund in the meantime protects you. Remember, building an emergency fund is a marathon, not a sprint – slow and steady wins here.

Put Your Cards to Work

Maximize your savings with your everyday spending. One clever way to build your emergency fund faster is to leverage your credit card rewards. Instead of letting cashback or points sit unused, funnel them into your emergency fund! This is where Kudos can help. Kudos is your ultimate financial companion, helping you effortlessly manage multiple credit cards, monitor your credit score, and maximize your rewards – all in one convenient platform.

Kudos shows you which card to use for each purchase to earn the most cashback or points. Those extra rewards can then be turned into extra dollars in your safety net. It’s a win-win: you continue your normal spending, but with Kudos’ smart recommendations, you earn more and boost your emergency savings without any extra strain on your budget. Add Kudos to your browser – it’s free – and watch your everyday spending start contributing to your emergency fund!

Where Should You Keep Your Emergency Fund?

You’ve worked hard to save this money – make sure to keep it in a safe, accessible place. The ideal spot for an emergency fund is an account that is easy to access quickly, low risk, and earns at least a bit of interest.

- High-Yield Savings Account (HYSA): This is the top choice for most people. A high-yield savings account is federally insured (up to $250k), so your money is safe, and it pays higher interest than a regular savings. You can withdraw funds easily transfer to checking when an emergency hits. Many online banks offer these accounts with no fees and significantly better interest (often several times the national average). Pro tip: Keep this savings at a different bank than your main checking – that way it’s out of sight (less temptation), but still only 1-2 days transfer away when needed

- Money Market Account: A money market account is similar to a savings account but sometimes comes with a debit card or check-writing privileges. It’s also FDIC-insured if at a bank. It can be a good option for an emergency fund if it offers competitive interest. The check-writing ability can be handy if you need immediate access, though you could usually just transfer to checking anyway.

- Cash (Small Amount): It’s smart to keep a small portion of your emergency fund in physical cash at home (in a secure place). This is for very immediate emergencies when electronic access might not work – think natural disaster scenarios or temporary bank outages. You don’t need a lot (maybe $100–$200 in small bills) – just enough for gas, food, or a hotel night if you can’t use your cards. The bulk of your fund should NOT be in cash under the mattress (it earns nothing and can be lost or stolen).

- Avoid Investing It: An emergency fund is not an investment – it’s insurance. Don’t put this money in stocks, mutual funds, or volatile assets like crypto. Why? Because you could lose value right when you need the money, or it may take time to sell and withdraw. Keep the fund in cash or cash-like accounts. (If you have extra savings beyond your emergency fund, that’s what you invest for growth.)

For most, a high-yield savings account is the best place. For example, if your emergency fund is $5,000, and your HYSA pays 4% APY, you’ll earn about $200 a year in interest – free money that can counteract a bit of inflation. Meanwhile, your money stays accessible and safe.

When (and When Not) to Use Your Emergency Fund

Congratulations – once you’ve built up an emergency fund, you have a financial superpower: liquidity. But using it requires restraint and good judgment. Here are guidelines on tapping your fund:

- Use it for True Emergencies Only: As discussed, only pull from it for genuine emergencies (urgent, necessary, unexpected). Before withdrawing, ask yourself, “Is this absolutely necessary? Can I cover it any other way without going into debt?” If it passes the test, use your fund confidently – that’s what it’s there for.

- Don’t Use it for Non-Essentials: Vacation shortfall? New gadget? Holiday shopping? Resist the urge to dip into the fund for these. Find other ways to budget for wants. Protect that emergency money like a nest egg.

- Replenish Asap: If you do withdraw from your emergency fund, make a plan to replenish it as soon as you’re able. After the dust settles on your emergency, treat refilling the fund as a top priority. For instance, if you used $2,000 from a $5,000 fund, direct extra savings in the following months toward that $2,000 until you’re back to full target. This way, you’re ready for the next emergency (because they often don’t politely wait a long time before striking again).

- Pair with Insurance/Other Resources: Remember, an emergency fund works alongside other safety nets. For big emergencies, insurance (health, auto, home) will cover some costs and your fund covers the rest or the deductibles. In some cases, if an expense is massive (beyond your fund), you might use your fund first, and then carefully consider other options like a low-interest loan or credit card as a backup. But having, say, $5k cash could prevent you from needing a high-interest loan for those first $5k of an emergency.

The bottom line: Guard your emergency fund for the real “uh-oh” moments in life, and it will guard you right back. When life happens, you’ll be so relieved to have this stash ready.

Bottom Line

Building an emergency fund is one of the best financial moves you can make for yourself. It’s not always easy – it requires patience and discipline – but even a small emergency fund can save you from huge financial trouble and stress. Start with a small goal and keep at it. Over time, you’ll create a buffer that turns potential money nightmares into mere inconveniences. In the journey to financial wellness, an emergency fund is your foundation. Begin laying that foundation today – your future self will thank you for it!

Emergency Fund FAQs

What’s the difference between a “rainy day fund” and an emergency fund?

A rainy day fund usually refers to a smaller pool of savings for expected but irregular expenses – think car maintenance, a vet bill, a minor home repair. It’s for the “rainy days” that will happen from time to time (but aren’t part of your routine budget). An emergency fund, on the other hand, is a larger amount saved for truly unexpected, costly events that can seriously upend your finances. For example, you’d use a rainy day fund if your laptop suddenly dies and you need a new one; but you’d tap your emergency fund if you lose your job and need to cover 3-6 months of bills. In short, rainy day funds are for small drizzles, emergency funds are for storms. It’s wise to have both: keep a modest rainy day fund so you don’t dip into your big emergency stash for trivial things.

Should I pay off debt or build an emergency fund first?

It’s a balancing act. You definitely want some emergency savings even if you have debt – otherwise an unexpected expense will just make you go deeper into debt. Many experts recommend first saving a starter emergency fund (say $500-$1,000) before focusing on extra debt payments. That small cushion handles minor surprises. After that, if you have high-interest debt (like credit card debt), it can make sense to pause growing the emergency fund and attack the debt – but still save a little each month if possible. Once high-interest debts are paid, you can fully focus on building 3-6 months of savings. Even while prioritizing debt, try to save something. For example, you might primarily direct money to debt, but put $25 a month into your emergency fund so it slowly grows. Bottom line: Have at least a starter fund first. Then, tackle toxic debt while keeping your safety net, and return to beefing up your emergency fund as soon as you can.

Is $1,000 enough for an emergency fund?

$1,000 is a great start – it covers many small emergencies, which already puts you ahead of a lot of people. In fact, only about 4 in 10 Americans could cover an unexpected $1,000 expense from savings, so if you have $1k saved, you’re doing well. However, $1,000 is generally not enough to handle bigger emergencies or a string of bad luck. It wouldn’t cover a month of rent in many cases, or a major car repair plus a medical bill in the same year. Treat $1,000 as a milestone, not the finish line. After hitting that target, aim for one month of expenses, then three months, and so on. Each extra cushion will protect you even more. So celebrate saving your first $1k – that’s huge – but then keep the momentum going!

Where should I keep my emergency fund money?

The best place is an account that’s safe and accessible. High-yield savings accounts are ideal for most people – they are FDIC-insured (so your money is safe up to $250k) and pay interest, and you can withdraw quickly when needed. An online savings account with a good interest rate and no fees is a popular choice. You could also use a money market account (similar benefits). Some people put part of their fund in a no-penalty CD or Treasury bills for slightly higher yield – that’s okay as long as you can cash out quickly without losing value. Avoid putting your emergency fund in stocks or other investments, and don’t lock it in a long-term CD that charges penalties (a 5-year CD, for example). And while keeping some cash at home (a few hundred dollars) for immediate needs is fine, don’t hold the whole fund in cash – it won’t earn interest and isn’t as secure. In summary, keep it liquid, safe, and earning a bit – a high-yield savings account is the one-size-fits-most answer.

Supercharge Your Credit Cards

Experience smarter spending with Kudos and unlock more from your credit cards. Earn $20.00 when you sign up for Kudos with "GET20" and make an eligible Kudos Boost purchase.

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)