Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

The Psychological and Financial Impact of BNPL on Gen Z

July 1, 2025

Buy Now, Pay Later (BNPL) services have become wildly popular among Gen Z and Millennials. They promise instant gratification – get what you want now, and pay for it in chunks over time. It’s easy to see the appeal: no hard credit checks, often no interest, and a simple, app-driven user experience. But as BNPL usage soars, questions arise about how it affects young consumers’ mindset and money.

This article explores the psychological draw of BNPL for Gen Z, and the potential financial pitfalls lurking beneath the shiny convenience. We’ll look at why BNPL feels different from credit cards, how it can influence spending behavior, and what the long-term impacts might be on Gen Z’s financial health.

Why Gen Z Loves “Buy Now, Pay Later”

It’s not your imagination – Gen Z has eagerly embraced BNPL. 51% of Gen Z (ages ~18-27) have used a BNPL service, according to a 2024 survey. That’s a huge adoption rate, rivaling or even overtaking credit card usage among young adults. What makes BNPL so attractive to this generation?

Instant Gratification, Delayed Pain:

Gen Z grew up in the age of one-click shopping and on-demand everything. BNPL fits right in. It lets you get that new outfit or gadget immediately, without waiting to save up the full amount. The pain of paying is spread out into smaller future payments, which feels less daunting. Psychologically, a $100 item doesn’t feel like $100 when you only have to shell out $25 now. This reduction in the perceived cost at the moment of purchase is a powerful motivator (and a classic recipe for impulse buying).

Budget-Friendly Appearances:

Many Gen Z users say they choose BNPL to better manage cash flow. In a survey, 42% of Gen Z BNPL users said they liked paying in installments to spread out the cost, and 34% appreciated knowing exactly what they owe each period and for how long. With BNPL, a purchase comes with a built-in payoff plan – e.g. “$25 every two weeks for 8 weeks.” For someone on a tight budget or irregular income, this can feel more manageable than a credit card bill that can fluctuate. BNPL offers predictability: you can mark those installment amounts on your calendar and plan around them. This structured approach might actually help some young consumers avoid blowing an entire paycheck at once, at least in theory.

Low (or No) Interest Temptation:

The fact that most BNPL short-term plans charge 0% interest makes them psychologically easy to justify. It doesn’t feel like taking on “debt” because you’re not paying extra for the privilege of paying later (again, as long as you pay on time). For Gen Z, who may have seen parents struggle with credit card interest, the interest-free aspect is huge. About 26% of Gen Z BNPL users cite the low or no interest as a key reason they prefer it. Essentially, BNPL is marketed as a savvy money move – “Why pay 100% now when you can pay 25% now and 75% later with no fees?”

Avoiding Credit Cards/Loans:

Many young adults are wary of credit cards and traditional loans. Whether it’s fear of getting into debt, distrust of banks, or simply lack of knowledge, some Gen Z hesitate to get a credit card at 18. BNPL provides an alternative way to buy on credit without a credit card. No lengthy applications, no credit score required in many cases, and no dealing with banks – all done through fintech apps that feel modern and user-friendly. It’s “credit” in a new, accessible form. As one article put it, Gen Z has a bit of a credit card “ick” factor, preferring debit and BNPL to plastic. BNPL fills that gap by offering a form of credit that doesn’t carry the same stigma for them.

Seamless Tech Integration:

BNPL is often baked right into shopping experiences. You’re on an online store, you go to check out, and you see an option: “Pay $25 now with Afterpay (4 installments)”. It’s hard to miss and often just a click or two to enroll. This lack of friction is key. Gen Z, being digital natives, are comfortable linking their card or bank account to a new app if it gives them a benefit. The BNPL providers also have sleek apps that track your payments and purchases, which can even give a (perhaps false) sense of control and organization. In contrast, applying for a credit card or personal loan feels like a separate, cumbersome process. BNPL meets Gen Z where they are – in the flow of shopping – which dramatically increases uptake.

The Psychological Downsides: BNPL and Overspending

While BNPL can feel empowering, it also comes with psychological traps. The very features that make it appealing can lead to financial strain:

Impulse Purchase Fuel:

Splitting payments makes things feel cheaper than they are. This can encourage impulse buying of items outside of one’s budget. The mindset becomes “It’s only $20 today, I can handle that,” ignoring the fact that four more $20 payments will follow. According to Bankrate, 25% of Gen Z BNPL users ended up regretting a purchase they made with BNPL – likely because they bought something they later realized they couldn’t comfortably afford. By lowering the upfront cost barrier, BNPL reduces the natural pause and reflection that larger purchases might otherwise trigger.

“Buy More, Pay Later” Snowball:

With multiple BNPL plans, it’s easy to lose track of how much you’ve committed to pay in total. You might have one plan for a clothing haul, another for new headphones, another for shoes – each $30 or $50 every two weeks. Individually, they seem manageable. But combined, you might have $200+ per month in BNPL payments without realizing it. One in three Gen Z BNPL users spent more than they should have, by their own admission. This overspending often happens because BNPL dilutes the awareness of the total spend. Psychologically, you focus on the installment amounts, not the grand total. It requires discipline to add up all those BNPL obligations and compare against your budget.

Easy to Overextend:

Unlike a credit card, where you have a set limit and the issuer might decline transactions beyond your capacity, BNPL providers each approve you in silos. So, you might get $500 credit with Afterpay, another $500 with Klarna, etc., even though no single lender sees the whole picture. There’s no central check on your overall debt load. The result: some consumers end up juggling numerous BNPL loans simultaneously, only realizing too late that the aggregate payments are too high. Because BNPL doesn’t typically show up on your credit report, even your future lenders (say, if you apply for a car loan) might not see that you have all these outstanding installment debts – a phenomenon dubbed “phantom debt”. This invisibility can be risky: you might qualify for more credit while already stretched thin due to BNPL commitments.

Less Pain Now, More Pain Later:

With BNPL, the pain of paying is delayed, but not eliminated. If you aren’t careful, by the time those later payments come due, you might be financially unprepared (especially if something changes like losing a job or an unexpected expense arises). The psychological term “present bias” comes into play – overvaluing the present (getting the item now) and undervaluing the future obligations. Young consumers, who may be new to managing bills, can get caught in a cycle of always paying for past purchases, leaving them short on cash for current needs. This can lead to a reliance on yet more BNPL or other forms of borrowing, creating a difficult loop.

Stress and Anxiety:

Initially, BNPL may feel stress-free compared to seeing a big charge on your credit card. But managing multiple payment schedules can create anxiety. Missing a BNPL payment often comes with a late fee and the stress of playing catch-up. 24% of Gen Z BNPL users have missed a payment, which can not only incur fees but also cause embarrassment or worry about falling behind. There’s also the concern of having your BNPL account frozen or being sent to collections if you default. In short, while BNPL can provide a short-term dopamine hit (new stuff! minimal immediate cost!), it can sow seeds of financial stress that sprout a few weeks later when bills are due.

Financial Consequences: What Happens When BNPL Goes Bad

From a purely financial standpoint, BNPL can be a double-edged sword for young consumers:

Fees and Penalties:

BNPL services make money in part by charging retailers a cut, but many also profit from late fees and other user charges. If you miss a payment, you might be charged a flat late fee (e.g. $10) or a fee capped at a percentage of the order value. Some services will even charge the fee and still expect the installment, effectively double-dipping your next payment. Unlike credit cards – which can charge late fees too – BNPL late fees can pile up if you have multiple plans. Imagine missing three BNPL payments across different apps; you could owe three separate fees. These penalties can quickly erase any benefit of using a “no interest” plan. Over half (56%) of BNPL users have run into some kind of problem, like overspending, missed payments, or return difficulties. For Gen Z living paycheck to paycheck, even a small fee can throw off their budget.

Bank Overdraft Domino Effect:

Many BNPL services auto-deduct installments from your debit card or bank account. If you miscalculate and don’t have enough in your checking account, a $25 BNPL charge could trigger an overdraft, leading your bank to slap on a $30-35 overdraft fee. Now you’re out $60 for that missed $25 payment. And you may still owe a BNPL late fee on top. A study aptly titled “Buy Now, Pay (Pain?) Later” found heavy BNPL users were more likely to incur overdraft fees. It’s a vicious cycle: BNPL can cause an overdraft, which then makes it even harder to pay the next BNPL installment.

No Credit Building, Possible Credit Damage:

Using BNPL responsibly doesn’t help your credit score, as we noted. But if things go wrong, it can hurt. Missed BNPL payments can be turned over to collections agencies, and at that point, they may get reported to credit bureaus, tanking your credit score. It’s the worst of both worlds: no upside for credit, but full downside if you default. And unlike a credit card, which might give you a chance to catch up with just a late fee, some BNPL providers might immediately disable your account or send defaults to collections faster. Young adults might not realize that even though BNPL feels informal, it’s still a legal debt obligation.

Opportunity Cost – Missing Out on Rewards:

There’s also a quieter financial impact: by using BNPL instead of a credit card, Gen Z shoppers are forgoing rewards they could have earned. As discussed in the previous article, no rewards or cashback from BNPL means if you spend, say, $1,000 via BNPL in a year (very easy to do), that’s $10-$50 in rewards you might have earned on a credit card – effectively money left on the table. Plus, without building credit, you might face higher costs later (like needing a co-signer for a loan or getting a higher interest rate because your score is lower than it could have been). These long-term costs are invisible but real.

Dependency and Financial Habits:

Perhaps the biggest long-term risk is developing a habit of relying on BNPL for routine purchases. If a young person gets used to splitting every other purchase into payments, they might not learn to budget for larger expenses or save up for wants. It normalizes living beyond one’s immediate means. The financial impact could be difficulty building savings (because future income is always spoken for) and a constant need for financing. It may also delay Gen Z from engaging with more beneficial financial products, like a credit card that, when used correctly, could provide more value.

How Gen Z Can Use BNPL Responsibly (and When to Avoid It)

Despite the risks, BNPL isn’t pure evil. It can be a useful tool if wielded carefully. Here are some tips for Gen Z to mitigate the negative impacts:

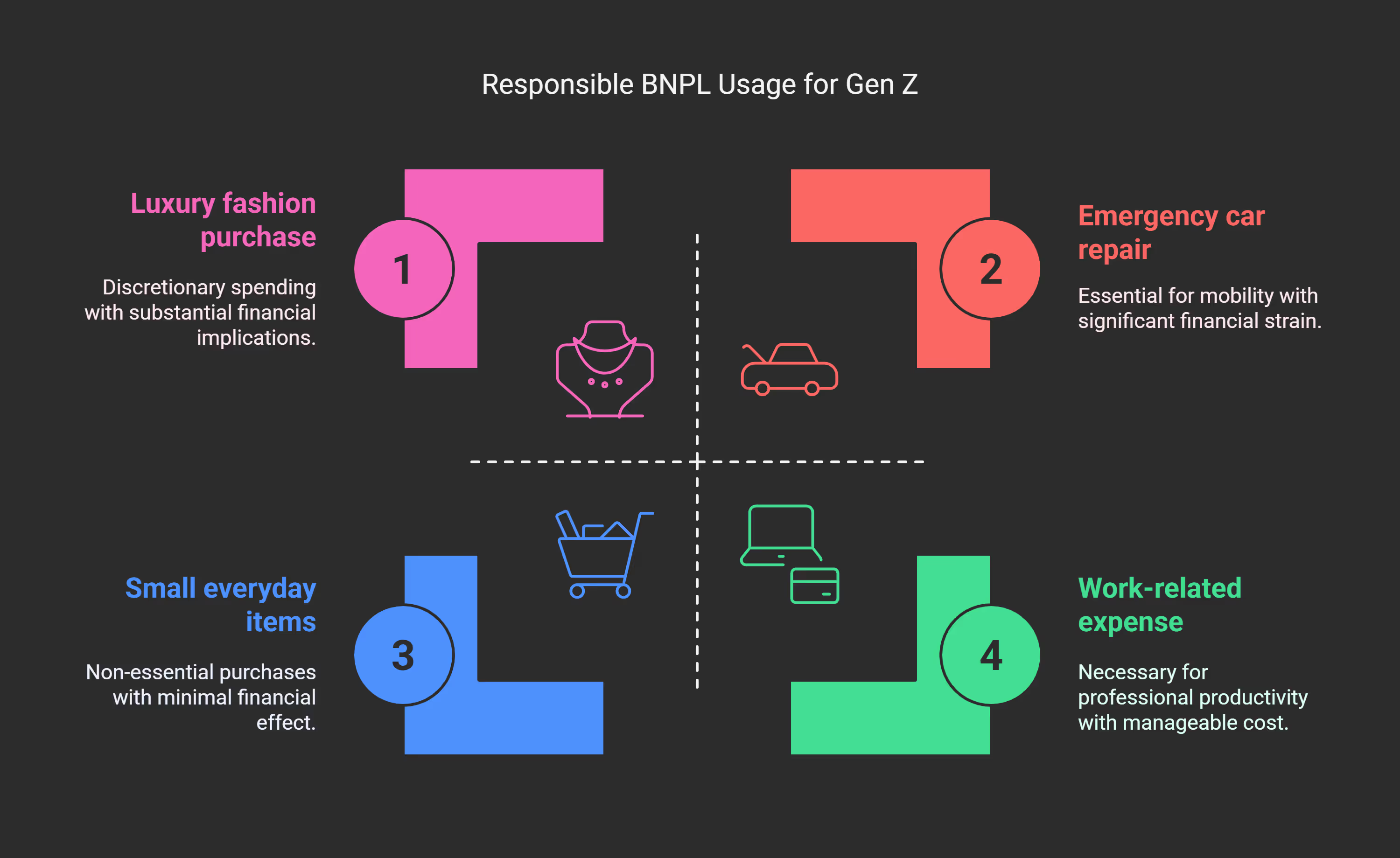

Reserve BNPL for Needs, Not Wants:

Ideally, use BNPL only for purchases that are necessary and time-sensitive. For example, emergency car repair, a work-related expense, or replacing a broken phone needed for communication. For discretionary or impulse wants (new gaming console, luxury fashion, etc.), think twice. If you wouldn’t take out a small loan for it, why use BNPL? Treat BNPL as you would any loan – because that’s what it is.

Limit the Number of Concurrent BNPL Plans:

A good rule of thumb is to have at most one BNPL at a time (or none!). If you already have an active plan, avoid starting another until the first is paid off. This prevents the juggling issue and keeps your deferred debt in one place. If you do have multiple, keep a clear list or use the BNPL apps’ calendars to track everything in aggregate.

Budget for BNPL Payments:

The moment you make a purchase with BNPL, incorporate those future payments into your budget. For example, if you agree to $50 every two weeks for two months, mark those $50 outflows on your calendar or budgeting app. Consider that money as already spent from your future income. One strategy: move the total purchase amount (minus the first payment) into a dedicated savings account right away. This way, when installments hit, you pull from that set-aside fund. It simulates the effect of having paid upfront (ensuring you actually have the funds).

Avoid Using BNPL for Everyday Small Purchases:

Some BNPL services now let you split even very small buys (like a $30 shirt). This is a red flag – if you need to split a $30 item, it might indicate cash flow problems. Try to restrict BNPL to bigger-ticket items that genuinely strain a single paycheck. Using BNPL on takeout food or clothes regularly is a sign it’s becoming a crutch. Remember, anyone can overspend, no matter the payment method – BNPL is not magic free money.

Understand the Terms:

Not all BNPL are 0% - some longer-term plans (6-12 months) through providers like Affirm may charge interest. Always check if there’s an APR or any fees. Also, know the late fee policy. Mark due dates with a reminder a day or two before (since many BNPL auto-charge, you want to ensure your payment method has funds). If your BNPL pulls from a debit card, consider having a small cushion in that account to avoid overdraft in case of timing issues.

Have an Exit Plan:

If you find yourself juggling BNPL payments and feeling overwhelmed, pause new purchases and focus on clearing existing balances. If needed, you could even consider consolidating – for example, using a 0% APR credit card to pay off BNPL (if possible) or a personal loan, effectively converting them into a single debt (though this requires discipline and good credit to execute). The goal is to break the cycle if it’s causing trouble.

Learn and Transition:

Use BNPL as a learning experience in managing installment credit. Over time, as you build confidence and maybe some credit history, consider transitioning to a credit card for greater benefits. If trust is an issue, start with a low-limit card so you can’t overspend too much. Use it like you used BNPL: for a purchase, then pay it off in set chunks (or immediately). Once you see that you can handle it, you’ll likely find the rewards and convenience of a credit card (one monthly payment, broader acceptance, perks) to be more rewarding than juggling multiple BNPL plans.

If you do start using credit cards more in place of BNPL, technology can help you stay on track. Kudos (the browser extension/app) not only helps maximize rewards but also helps manage multiple cards responsibly. You can see all your cards in one place, track your spending, and get reminded which card to use where. It’s like a personal finance coach in your pocket, tailored for Gen Z’s digital lifestyle. And when you sign up with GET20, Kudos gives you $20 – a nice head start toward your next statement payment or a little reward treat for yourself. Using tools like this can ease the transition from the BNPL habit to a more rewards-rich, credit-building strategy, all while keeping you responsible and informed.

FAQs: BNPL’s Impact and How to Navigate It

Is Buy Now, Pay Later really that different from using a credit card?

In practice, BNPL and credit cards both let you buy now and pay later – but the experience and implications differ. BNPL splits a single purchase into a fixed number of payments, often with no interest, and usually doesn’t report to credit bureaus. A credit card lets you revolve many purchases and only requires a small minimum payment each month (very flexible, but that flexibility can lead to long-term debt with interest). Psychologically, BNPL feels more structured and finite – you know a purchase will be paid off in, say, 8 weeks. A credit card is open-ended; if you only pay minimums, you could be paying off that purchase for years. Also, BNPL is integrated at checkout, making it more of an on-the-spot decision, whereas deciding to put something on a credit card might involve an after-the-fact decision of whether to carry a balance.

Does BNPL lead to people spending more money than they normally would?

Yes, it can encourage overspending. Studies and surveys have found a significant number of BNPL users spend beyond their means. For example, around one-third of Gen Z BNPL users admitted to spending more than they should have because of BNPL. By lowering the immediate cost barrier, BNPL lowers our psychological guard. It’s easier to say “yes” to upgrades or unnecessary purchases when the price tag’s impact is delayed. The effect is similar to how credit cards can lead to higher spending than cash (because you’re not feeling the hit immediately), but BNPL can be even more sneaky since even the first payment is just a fraction. The best defense is self-awareness: treat BNPL purchases as if the full amount is still coming out of your account (because it will, just in parts). If you wouldn’t be comfortable putting the full amount on your debit card today, reconsider the purchase.

What happens if I can’t pay a BNPL installment on time?

If you miss a BNPL payment, a few things could happen. Most providers will charge a late fee immediately or after a grace period. The fee can be a flat amount (commonly $5-$10) or a percentage of the installment. They will likely try to charge your payment method again. Some BNPL companies might stop you from using them for new purchases until you catch up. If you continue missing payments, the account could be sent to a collections agency, which is serious – it could show up on your credit report and damage your credit score. Unlike credit cards, where a single missed payment might not be reported until 30 days past due, BNPL doesn’t have the same reporting standards, but they reserve the right to report defaults.

Also, you’ll still owe the remaining payments. Long story short: don’t miss BNPL payments if at all possible. Set reminders or enable auto-pay. If you truly can’t make a payment, contact the BNPL provider – some have hardship policies or can extend the term. Avoiding communication can fast-track your account to collections.

Are there any benefits to BNPL on big purchases versus using a credit card?

BNPL can be beneficial for a big purchase if you don’t have a credit card or your card’s limit is too low to cover the purchase, or if the credit card’s interest would kick in and you can’t pay it off quickly. For example, if you have a $800 emergency expense and no savings, putting it on a credit card could incur interest if you can’t pay it off soon. A BNPL plan might split it into 4×$200 with no interest, which is easier to manage over two months.

So it can serve as a useful short-term financing tool without interest costs. Also, if you’re worried about maxing out your credit utilization (which can temporarily ding your credit score), using BNPL won’t affect your utilization ratio since it’s not reported. However, remember that many credit cards offer 0% APR promotions for big purchases too – if you have access to one, that could be even better (you’d get the interest-free period and rewards/consumer protections). If a merchant offers a special BNPL promotion (like “No payments for 3 months” or a longer plan at 0%), that could also be a draw.

How is Gen Z’s credit outlook affected if they prefer BNPL over credit cards?

If Gen Z as a whole continues to favor BNPL and delay using credit cards or other credit-building products, we might see a scenario where many young adults have thinner credit files. A credit score is built by having accounts like credit cards, loans, etc., and demonstrating good payment history. If a 22-year-old has made dozens of BNPL purchases but never had a credit card or loan, by age 25 they might still have no credit score or a very limited history. This can make it harder (or more expensive) when they want to finance something larger, like a car, or even when renting an apartment (landlords check credit). Some banks are starting to incorporate alternative data (like BNPL records or bank account history) to evaluate creditworthiness, but it’s not widespread yet.

On the flip side, if Gen Z avoids bad credit card debt by using BNPL carefully, that could be positive – they’re not racking up high-interest debt early on. The ideal might be a balance: use credit cards lightly to build credit and earn rewards, while using BNPL sparingly for convenience. If Gen Z can manage that balance, their credit outlook can remain healthy. But if they ignore credit building entirely, they could face hurdles. The good news is that some BNPL providers are exploring reporting positive payment history to bureaus in the future. Until then, it’s wise for Gen Z to eventually get into the credit system through a low-risk product (like a starter credit card or credit-builder loan) so they aren’t at a disadvantage later.

Supercharge Your Credit Cards

Experience smarter spending with Kudos and unlock more from your credit cards. Earn $20.00 when you sign up for Kudos with "GET20" and make an eligible Kudos Boost purchase.

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)