Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

What Credit Score Do You Need to Buy a House?

Buying a home is a major milestone – and your credit score plays a huge role in making it happen. Mortgage lenders use your credit score to gauge how risky it is to loan you money for a house. So, what credit score is needed to buy a house? The short answer: it depends on the type of mortgage, but generally at least in the low 600s for a conventional loan.

In fact, minimum credit score requirements can range from 500 up to 700, depending on the loan program. Having a higher score not only improves your chances of approval, but also helps you snag better interest rates and save money over the life of your loan. Let’s break down the details.

Minimum Credit Score Requirements by Mortgage Type

Mortgage programs have different minimum credit score rules. Here’s an overview of common loan types and the approximate minimum FICO scores needed for each:

Conventional Loan (Conforming):

Typically 620+ minimum. Conventional mortgages (those that meet Fannie Mae/Freddie Mac standards) usually require at least a 620 FICO score. Some lenders might even want 640 or 660+. A higher score (e.g. 740+) can help you qualify for better rates.

Jumbo Loan:

Around 700+. Jumbo loans (for amounts above conforming limits) have stricter requirements – often a 700 minimum score – since lenders take on more risk with a larger loan.

FHA Loan:

500 or 580, depending on down payment. FHA-insured loans allow credit scores as low as 500 if you put at least 10% down; otherwise you’ll need 580+ for the minimum 3.5% down payment. This makes FHA loans popular for buyers with fair or even poor credit.

VA Loan:

620+ typically. The VA (Veterans Affairs) doesn’t set an official minimum, but most VA lenders require around a 620 FICO. VA loans are available to qualifying veterans and active-duty service members with zero down payment.

USDA Loan:

580–640. USDA rural home loans have no government-set minimum, but lenders commonly look for at least 580 (some require 620 or 640). These offer zero down financing for eligible rural or suburban homebuyers.

Other Programs:

Some first-time buyer programs or subprime lenders might accept lower scores in special cases, but expect higher rates. Conversely, excellent credit (760+) opens doors to more options and the lowest rates.

As you can see, you don’t necessarily need an 800 credit score to buy a house – far from it. Even a score in the high-500s might secure an FHA loan. However, scores below 600 will limit your choices to government-backed loans (FHA/VA/USDA), since conventional mortgages won’t approve such borrowers.

Generally, aiming for at least a 620 will give you more loan options, and getting into the 700s will significantly improve your interest rate and terms.

Why a Higher Credit Score Matters for a Mortgage

Meeting the minimum score gets your foot in the door, but higher credit scores get rewarded in the mortgage world. Lenders price loans based on risk – if your score is on the low end, they’ll often charge a higher interest rate to compensate.

For example, as of mid-2024, borrowers in the 620-639 FICO range were seeing average 30-year mortgage rates around 7.8%, whereas those in the 760+ top tier enjoyed roughly 6.2%. That difference in interest can cost you tens of thousands more over the life of a loan.

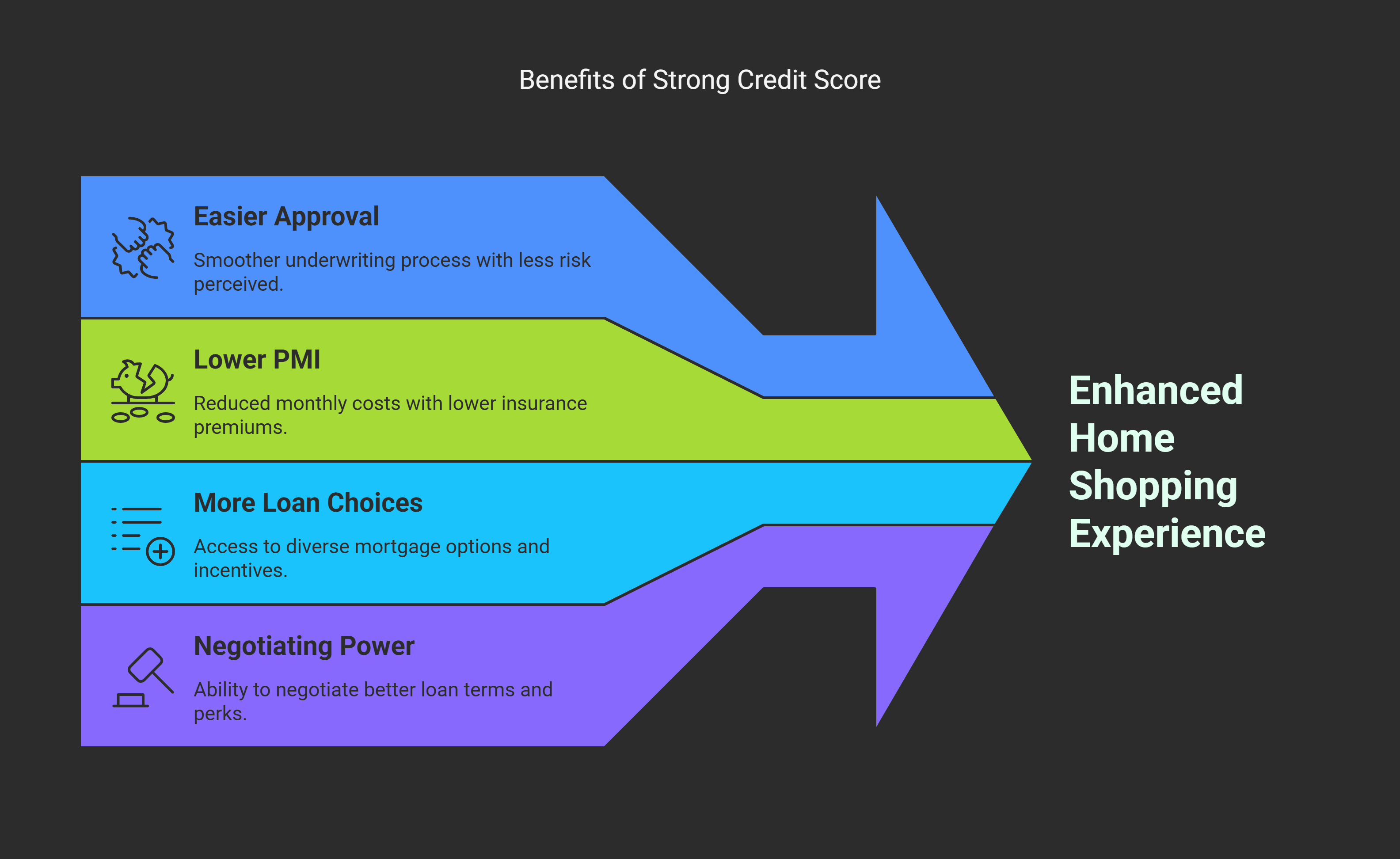

In addition to interest savings, here are other benefits of having a stronger credit score when home shopping:

- Easier Approval: Lenders view you as a less risky borrower. You’re more likely to get through underwriting smoothly, even if you have a higher debt-to-income ratio or a smaller down payment.

- Lower Private Mortgage Insurance (PMI): For conventional loans, if your down payment is under 20%, you’ll pay PMI. A higher credit score can reduce PMI premiums, saving you money each month.

- More Loan Choices: With good credit, you might qualify for more types of mortgages (such as conventional, jumbo, or specialty programs) and even get special incentives from lenders. Borrowers with scores under ~620 have very limited choices (mostly FHA).

- Negotiating Power: A strong credit profile could give you leverage to negotiate closing cost credits or other perks from lenders eager to have your business.

In short, while you can buy a house with a middling credit score, there are big advantages to boosting your score before you apply. Even moving from a 650 to a 720 could shave a chunk off your interest rate and monthly payment.

Can You Get a Mortgage with Bad Credit?

“Bad” credit (usually defined as a score below 580) makes home buying challenging, but not impossible. Thanks to programs like FHA, there are paths to homeownership for those with damaged credit. FHA loans, for instance, allow FICO scores down to 500, and some specialty lenders offer non-prime mortgages to sub-580 borrowers. VA loans and USDA loans technically have no minimum FICO (some lenders might go into the 500s on a case-by-case basis).

That said, there are important caveats:

- You’ll Need a Bigger Down Payment: FHA applicants with sub-580 scores must put at least 10% down. Other low-credit options may require larger down payments or cash reserves to offset risk.

- Higher Rates and Fees: A poor credit mortgage will come with a higher interest rate. Even a FHA loan adds extra fees (upfront and annual mortgage insurance) that will be pricier for lower-score borrowers. Over 30 years, the cost difference is substantial.

- Limited Loan Sizes: Lenders might cap the amount you can borrow if your score is very low. Combined with the higher rates, this could limit the price of homes you can afford.

- Manual Underwriting: You might go through a stricter review (called manual underwriting) where the lender scrutinizes your finances beyond just the credit score – they’ll want to see steady income, low debts, and explanations for any past credit issues.

In practice, few borrowers actually get mortgages with scores under 600 – they represent a small fraction of loans originated. If your score is in the “bad” range, it may be wise to improve your credit first (more on that below) before taking on a mortgage. However, if you’re close (say 590-600), talking to an FHA-approved lender could clarify your chances.

Important: Be wary of “buy a house with no credit check” offers. Legitimate lenders will check credit. If you’re considering owner financing or rent-to-own because of bad credit, tread carefully and understand the risks.

How to Improve Your Credit Score Before Buying a Home

If your credit score isn’t where you want it, the good news is that scores aren’t static – you can improve them over time. Before applying for a mortgage, take some months (or longer, if needed) to polish your credit profile.

Here are actionable steps:

Check Your Credit Reports:

Pull your reports from all three bureaus (Equifax, Experian, TransUnion) at annualcreditreport.com – it’s free weekly. Look for errors or negative items you can address. Dispute any inaccuracies you find, as removing them could boost your score quickly if they were significant.

Pay Down Credit Card Balances:

Your credit utilization (the percentage of your credit limits you’re using) has a big impact on scores. Try to pay down existing card balances to under 30% of the limit (under 10% is ideal). For example, if you have a $5,000 limit card, keep the balance under $1,500. This can potentially raise your score within a couple of billing cycles.

Catch Up on Any Late Payments:

Payment history is the number one factor in your score. If you have any past-due accounts, bring them current as soon as possible. One 30-day late can drop your score significantly, so prioritize never missing payments. Set up autopay or reminders for all bills.

Avoid New Credit Applications:

Each new credit inquiry can ding your score slightly, and opening new accounts could lower your average account age. In the lead-up to a mortgage, don’t open new credit cards or loans unless absolutely necessary. (This includes refraining from financing new furniture or a car until after your home loan is secured.)

Build Positive Credit History:

If you have limited credit, consider opening a credit card (or becoming an authorized user on someone else’s card) well ahead of your home purchase to build history. Just be sure to use it lightly and pay on time. A tool like Kudos can help you find a card that fits your credit profile and monitor your progress as you build credit responsibly – all in one place.

Pay Off Small Debts or Collections:

If you have any collections or outstanding debts, paying them off might help (though older collections may not boost your score, some newer scoring models do weigh paid-off collections more favorably). Also, reducing overall debt will improve your debt-to-income ratio, which lenders check alongside your credit score.

Keep Old Accounts Open:

Length of credit history matters. Don’t close your oldest credit card even if you don’t use it much – having that long, positive history helps your score. Use it occasionally for a small purchase to keep it active.

It’s also smart to avoid big financial changes during the home-buying process. Once you begin applying for mortgages, hold off on changing jobs, making large, unusual deposits, or taking out other loans. Stability is key. Many lenders will re-check your credit right before closing – you don’t want a new surprise (like a new car loan or a maxed credit card) to derail your mortgage at the last minute.

How Your Credit Card Habits Affect Your Mortgage Readiness

Most homebuyers will have one or more credit cards, and how you manage them can make or break your credit score. Here are a few pointers on aligning your credit card strategy with your homeownership goals:

Keep Balances Low:

As mentioned, try to pay off your cards in full each month. If that’s not feasible, at least reduce balances below 30% of your limit before your statement closes (and definitely before applying for a mortgage). This lowers your utilization ratio reported to credit bureaus.

Continue Paying On Time:

A single missed credit card payment can drop your FICO score by 100+ points, especially if your credit was good to start. Set up automatic minimum payments so you never accidentally miss one. Consistent on-time payment history will strengthen your score and impress underwriters.

Don’t Close Cards Right Before Applying:

Even if you’ve paid off a card, keep the line open (unless it has a high annual fee and you’re done with it). Closing can’t remove the history immediately, but it will eventually and could slightly hurt your utilization. Lenders also like to see that you can handle multiple credit lines responsibly over time.

Avoid Large Purchases on Credit:

Charging a big vacation or buying expensive appliances on your credit card right before or during the mortgage process can spike your utilization and monthly obligations. Hold off on those big charges until after you close on your home. If you must make a large purchase, consider using savings or waiting.

Consult Your Lender if Unsure:

If you’re not sure how a financial move might affect your approval, ask your lender. For example, should you pay off an installment loan or credit card to qualify? Sometimes paying down a credit card can boost your score quickly. A lender or a tool like Kudos (which offers personalized credit insights) can help prioritize actions that move the needle.

Remember, your goal is to present the cleanest, strongest credit profile to the mortgage underwriter. Responsible credit card use is a big part of that. Many future homeowners find it helpful to use technology like Kudos – an AI-powered browser extension – which can track your credit score, remind you of payments, and even suggest the optimal card for each purchase to maximize rewards without harming your credit. It’s like having a financial coach that ensures you’re earning points for that future furniture shopping and staying mortgage-ready at the same time.

FAQ: Credit Scores and Homeownership

What credit score is needed to buy a house with no money down?

It depends on the loan program. VA loans (for veterans) and USDA loans (for rural areas) allow 0% down financing. While the VA and USDA don’t set hard credit score minimums, lenders typically want about a 620 FICO or higher for these zero-down loans. Some VA lenders may approve slightly lower scores on a case-by-case basis.

Can I get a mortgage with a 600 credit score?

Possibly – a 600 score is below the cutoff for most conventional loans, but it’s in range for an FHA loan. FHA guidelines permit scores as low as 580 with a 3.5% down payment. With a 600 score, you’d likely qualify for FHA (assuming your finances meet other criteria). You’d need to put at least 3.5% down, and you’ll pay FHA mortgage insurance. Some lenders might also do VA loans around that score if you’re eligible.

Do mortgage lenders use my FICO or VantageScore, and which version?

Mortgage lenders almost universally use FICO scores for underwriting (not VantageScore). In fact, they often use older FICO models specific to mortgages – commonly FICO Score 2, 4, or 5 from each bureau (also known as “classic” FICOs). These can differ from the newer FICO 8/9 or the score you see in your banking app. However, there are changes on the horizon: the FHFA has approved newer models FICO 10T and VantageScore 4.0 to be used by mortgage lenders in coming years, which consider factors like trending credit data. Tools like Kudos can help you monitor your credit so there are no surprises when the lender checks your scores.

How much will my credit score drop when I get a mortgage?

It’s normal to see a small, temporary dip in your credit score after taking out a mortgage. The hard inquiry from the application might shave off a few points (typically less than 5). Also, a new mortgage is a large installment debt, which can lower your score slightly until you build some payment history. On average, people might see a drop of 5–20 points. The good news: as you make on-time mortgage payments, your score should recover and even improve over time.

Should I pay off my credit cards before applying for a home loan?

Yes, paying down credit cards can be very beneficial before applying for a mortgage. Lower credit card balances reduce your credit utilization, which can raise your credit score and improve your debt-to-income ratio. Both are positives for a mortgage application. You don’t necessarily need to zero out every card (and you don’t need to close them), but the less outstanding revolving debt, the better. Prioritize paying off high-interest cards first. If you have limited funds, aim to get each card balance below 30% of its limit.

Double the Cash, Zero the Worry

Looking for consistent rewards without the hassle? The Citi Double Cash® Card rewards you twice: 1% when you buy, another 1% when you pay—for a total 2% cash back on every purchase with no categories to track. Plus, smart balance transfer options help you take control of existing debt. Simple, powerful, perfect for today's savvy spenders.

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)

%20(1).webp)