Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

What Factors Affect Your Home Insurance Rates?

July 1, 2025

Introduction

Ever wonder how your homeowners insurance company decides what to charge you? You’re not alone. Home insurance premiums can feel mysterious, but they actually boil down to a set of key risk factors. Some of these factors are about your home itself.

In this 2025 guide, we’ll break down the main factors that affect your home insurance rates. Understanding these will help you see why your quote is high or low, and what (if anything) you can do to get a better deal. Let’s demystify your home insurance premium!

1. Location of Your Home

“Location, location, location” isn’t just a real estate mantra – it’s huge for insurance too. Insurers care where your home is because location correlates with the likelihood of certain risks.

Here’s how location factors in:

- Climate and Natural Disasters: If you live in a region prone to hurricanes, tornadoes, earthquakes, or wildfires, expect higher rates.

- Crime Rates: Homes in neighborhoods with high crime or burglary rates may face higher premiums.

- Fire Services and Hydrants: How close is your home to a fire station or fire hydrant? Insurers actually check this. If you’re within a certain distance, you get better rates because if a fire happens, help can arrive faster.

- Local Building Costs: Insurance covers rebuilding costs if your home is destroyed. If you live in an area where construction labor/material is very expensive, your dwelling coverage costs more.

- Litigation Environment: Subtler factor, but some states are more prone to insurance litigation or have different regulations, which can raise insurers’ costs.

You can’t change your location (unless you move!), but you should be aware that it plays a major role. When comparing yourself to a friend in another state, location might be why your insurance cost differs even if your homes are similar.

2. Home Characteristics and Condition

The specifics of your house itself heavily influence your premium:

Rebuilding Cost (Home Value)

The size of your home, its square footage, and features determine how much it would cost to rebuild. A large 4,000 sq. ft. house will cost more to insure than a 1,200 sq. ft. cottage, because there’s more to replace in a total loss. High-end finishes also increase the insured value. Insurers often calculate a replacement cost based on your home’s details – the higher that number, the higher your premium since they’re on the hook for more in a claim.

Age of the Home

Older homes tend to have higher premiums. Why? Older wiring or plumbing can be riskier. Also, if a very old home has unique construction (plaster walls, antique features), it can be pricier to repair. On the other hand, a newly built home often enjoys lower rates and even a “new home discount,” since new systems are safer and up to code.

Building Material

What’s your home made of? Wood frame houses are riskier for fire than brick or masonry houses. If your home is primarily brick or masonry, some insurers give a discount because it’s more fire-resistant. Conversely, if you have a log cabin (wood construction, high combustibility), you might pay more.

Roof Condition and Material

The roof is one of the most important parts of your house for insurance. A newer roof can earn you a discount. Certain materials like metal or tile roofs that are more resistant to fire or hail can also lower rates. Insurers know that in many claims, the roof is what gets hit. If yours is old or in poor shape, it’s a higher risk. Some companies even won’t cover a roof beyond a certain age without inspection or a premium surcharge.

Safety Features

Homes equipped with things like smoke alarms, security systems, sprinkler systems, storm shutters, impact-resistant glass, etc., often get credits on insurance. These features either reduce the chance of a loss or reduce the severity. They might not drastically cut the premium, but every bit helps. Modern homes often come with many of these built-in, which is why newer homes can be cheaper to insure.

Special Features

Swimming pool? Trampoline? These can increase your liability premiums because of injury risk. A pool typically raises your liability cost a bit, and insurers may require you to have a fence or other safety measures. Likewise, certain dog breeds or having a home business can influence coverage. If you have a specific concern, you may need a specialty insurer or rider.

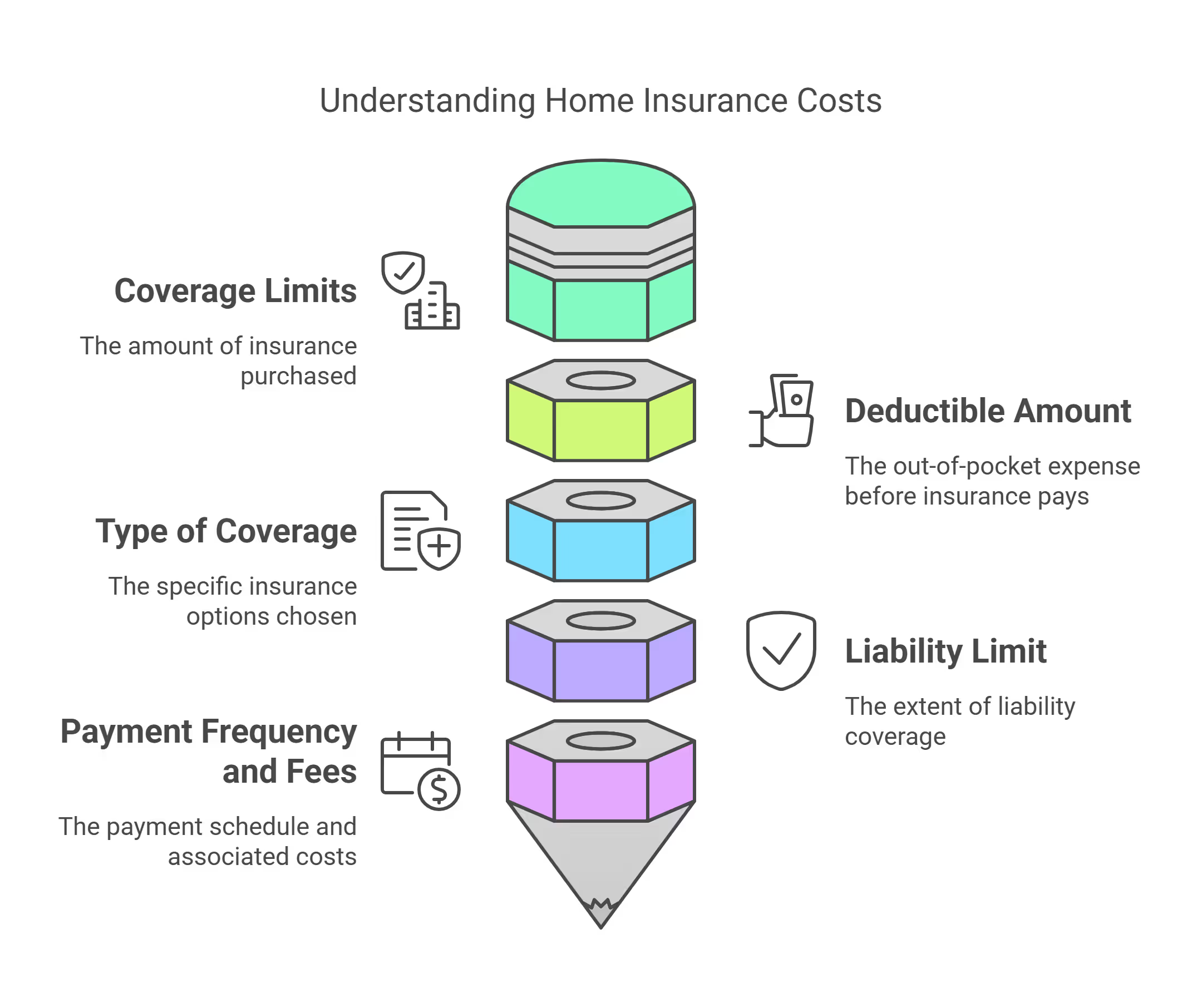

3. Coverage Choices (Policy Details)

Factors not just about your home, but about how you set up your insurance policy will affect the price:

Coverage Limits

Simply put, the more coverage you buy, the more it costs. If you insure your home for $500,000 versus $300,000, you’ll pay proportionally more. Same goes for personal property coverage – if you opt for higher limits to cover expensive belongings, premium goes up. It’s important to have enough coverage, but if you have a lot of “extras” you don’t need, trimming can save money.

Deductible Amount

This is a big one you do control. A deductible is what you pay out-of-pocket on each claim before insurance pays the rest. Common deductibles are $500, $1,000, $2,500, etc. Choosing a higher deductible lowers your premium because you’re essentially agreeing to shoulder more of any potential loss.

Type of Coverage

There are different forms of home insurance and options like replacement cost vs. actual cash value for your belongings. A policy that will pay full replacement cost on everything is more expensive than one that pays depreciated value. Also, adding endorsements all raise the premium. Tailoring your policy to what you need (and skipping what you don’t) can affect price.

Liability Limit

Most homeowners policies come with $100k or $300k liability coverage by default. Increasing that to $500k or $1 million will slightly increase your premium. If you have a lot of assets, it’s wise to carry higher liability. But strictly speaking, if someone is looking to cut cost, they might stick to a lower liability limit.

Payment Frequency and Fees

Some insurers charge a bit more if you pay monthly vs. annually. Paying in full can sometimes net a small discount. Also, opting for paperless billing and auto-pay often gives a ~$5-10 discount with many companies.

4. Your Personal Factors (Claims & Credit)

Now it’s time to talk about you, the homeowner. Two big personal factors are in play: your claims history and your credit-based insurance score.

- Claims History: If you’ve filed home insurance claims in the past (usually within the last 5 years), insurers may view you as more likely to have future claims. Each claim can nudge your premium up.

- Credit Score: Yes, surprisingly to some, your credit score can affect your home insurance premium (except in states that forbid it). Insurers use a credit-based insurance score derived from your credit history as a rating factor. Statistically, people with lower credit scores file more claims, so insurers charge more to those folks.

- Note: In a few states (California, Maryland, Massachusetts for home insurance), credit can’t be used, so in those places, this factor drops out. But in the majority of states, it’s influential.

- Other Personal Info: There are a few other odds and ends. Some insurers consider your occupation or education level as a factor (there are affinity discounts for teachers, engineers, etc., implying some professions are lower risk customers). Your marital status can matter – statistically married people file fewer claims, so you might see a slight benefit if you’re married.

6. How Insurers Weigh These Factors (The Secret Sauce)

Every insurance company has its own “secret recipe” for how they weigh and combine all the above factors. That’s why you get different quotes from different insurers for the same home. One company might put a heavy emphasis on credit and claims history, while another cares a bit more about the home’s age and location.

This is why shopping around is so crucial – you might find that Company X is a perfect fit because it favors the factors you’re strong in and downplays the ones you’re not. Company Y might be the opposite, and thus quote higher. It’s also worth noting insurers continuously update their models. What was a good rate last year might creep up, and another company might become more competitive.

As a homeowner, it’s wise to re-shop your insurance every year or two. This doesn’t mean you must switch often, but it keeps them honest – and you’ll know if you’re overpaying relative to what the market offers for your risk profile.

Conclusion

Your home insurance premium isn’t just a random number – it’s the sum of a bunch of factors about you and your home. To recap, major things that affect your rate include: where you live, the characteristics of your home (age, construction, replacement cost), the coverage options you choose, your personal claims and credit history, and any discounts you can leverage. Some of these you can’t change (you won’t move house just for insurance). But others you can influence.

If your premium seems high, review the factors above and see if any red flags stand out (did you have multiple claims? Is your credit score low? Is your coverage too high for what you need?). Then you’ll know what to address or ask your insurer about. Being informed puts you in the driver’s seat – you can make tweaks to lower your risk profile or shop around for an insurer that favors your situation.

Home insurance is all about managing risk – both for you and the insurer. By understanding how insurers view risk, you can better manage your own insurance costs. Hopefully, this guide helped clarify that.

FAQs

What are the most important factors that determine home insurance cost?

The biggest factors usually are: the home’s location (geography and disaster risk), the replacement cost of the home (home value, size, construction), the coverage and deductible you choose, your claims history, and your credit score (in most states).

Why did my homeowners insurance go up this year even though I didn’t make any claims?

It can be frustrating, but a few reasons: inflation in construction costs (if lumber, labor, etc. got more expensive, your coverage limit might increase and so does premium), overall increase in claims in your area (maybe there were more wildfires or storms regionally, so all rates went up to cover those payouts), or changes in your insurer’s formula (they might have adjusted how much credit score or something affects rates).

Does having a mortgage vs. no mortgage affect my insurance rate?

Not directly for the rate itself. Insurance companies don’t charge you more or less based on having a mortgage. However, if you have a mortgage, the lender will require you carry insurance, but that doesn’t change pricing.

Will installing a security system really lower my home insurance?

In most cases, yes – albeit modestly. Almost all insurers give a discount for a monitored burglar alarm (one that alerts an external center or police). The discount might be around 5%. Fire alarms and sprinkler systems can also yield discounts in that range. So, if your premium is $1,000, a 5% discount is $50 – not huge, but something. More importantly, it gives peace of mind and could prevent a theft claim which would hike your premiums.

How can I lower my home insurance premium?

Several ways: shop around to make sure you’re not overpaying with your current insurer; increase your deductible if you can afford a higher out-of-pocket in emergencies; bundle your home and auto insurance for a multi-policy discount; claim all discounts (alarm systems, sprinklers, loyalty, new roof, etc.); avoid filing small claims (to keep your claims-free discount intact); and improve your credit score over time to move into a better rating tier.

Supercharge Your Credit Cards

Experience smarter spending with Kudos and unlock more from your credit cards. Earn $20.00 when you sign up for Kudos with "GET20" and make an eligible Kudos Boost purchase.

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)