Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

When and Why You Should Cancel Your Credit Card

July 1, 2025

Canceling a credit card is a significant decision that can have both pros and cons for your financial life. You might be asking yourself: “When should I cancel a credit card, if ever?” Perhaps you have a card with an annual fee you’re no longer willing to pay, or you have too many cards and want to simplify. Maybe you’re concerned about overspending and think closing a card will remove temptation. All of these can be valid reasons. However, it’s crucial to weigh those reasons against potential downsides like impacts on your credit score.

In this guide, we’ll break down when and why you should cancel a credit card (and when you shouldn’t), how to go about canceling in a safe way, and how to mitigate any negative effects. By the end, you’ll know if canceling your card is the right move for you and the steps to do it properly.

Good Reasons to Cancel a Credit Card

While keeping cards open is generally beneficial for credit, there are scenarios where canceling a card makes sense:

- The card has an annual fee you can’t justify. If you’re paying a high annual fee for a card that no longer provides value to you, cancelling might be wise. Perhaps the card’s rewards or perks don’t fit your lifestyle anymore, and there’s no suitable downgrade option. Why keep paying, say, $95 or $550 each year for benefits you don’t use? In this case, canceling stops the financial bleed. (Tip: Before you cancel, see if the issuer will waive the fee or offer a retention bonus – but if not, letting the card go could be the best choice.)

- You have a pattern of overspending on that card. If a particular credit card is fueling bad spending habits or debt, sometimes cutting it off is healthier. For example, if you’ve struggled with keeping a balance or overspending because that card has a high limit, cancelling it can remove the temptation. Your financial well-being comes first. Some people literally cut up the physical card to avoid using it (as pictured above). Closing the account ensures you won’t rack up new charges on it.

- You have too many credit cards to manage. Maybe you’ve accumulated a wallet full of cards over the years. Juggling multiple due dates, reward programs, and accounts can be cumbersome. If certain cards aren’t providing value and are just adding complexity, canceling one or two can simplify your financial life. Focus on a few cards that serve your needs best. It’s better to manage a curated set of cards responsibly than to be overwhelmed with accounts.

- You’re switching banks or rewards programs. Perhaps you’ve decided to streamline to one bank or you’ve moved your loyalty to a different airline/hotel. If an old card doesn’t fit your new strategy, you might drop it. For instance, if you’ve stopped flying a certain airline, their co-branded card might not be worth keeping (especially if it has a fee). As long as dumping it won’t hurt your credit too much (check the factors below), you can consider closing it.

- To avoid potential credit risks before a big loan. This one is less obvious: If you plan to apply for a major loan (like a mortgage), sometimes having too much available credit can worry lenders during manual underwriting. In some cases, people cancel an unused card or two before a mortgage application to show they have less available credit line (reducing the theoretical risk of taking on new debt). This is situational and you’d only do it if a loan officer suggested it, but it’s a possible reason to close an account.

- The card was fraudulently opened or you simply never use it. If you have a card you never wanted in the first place (e.g. an account opened fraudulently in your name) or a card that you haven’t touched in years, canceling is sensible. Unused cards could be closed by the issuer eventually anyway, but you taking the initiative allows you to control the timing and ensure it’s done securely. An inactive card with no annual fee isn’t a big burden to keep open (and might even help your credit), but if you truly want it gone, you can close it.

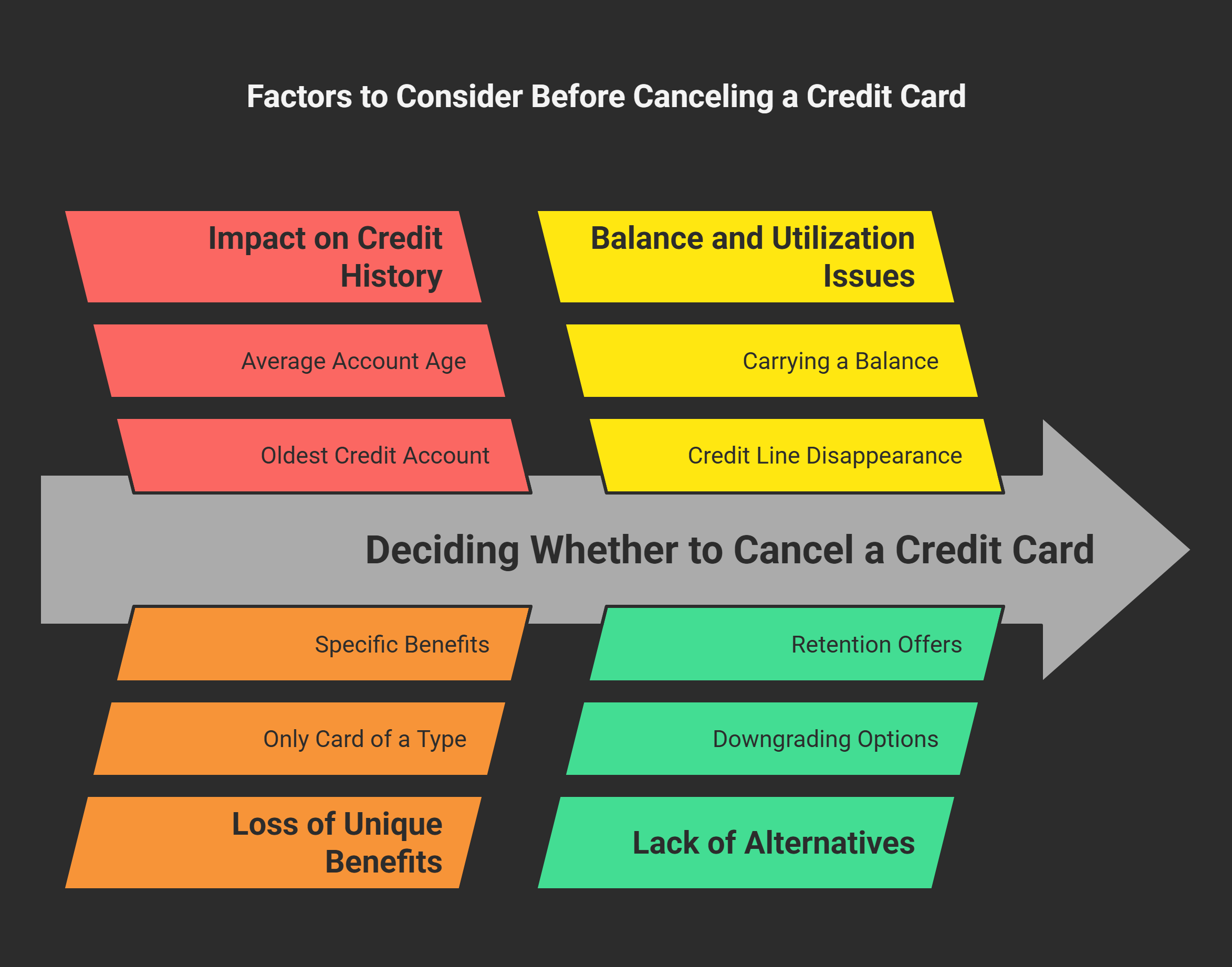

When to Think Twice About Canceling

Before you rush to close an account, consider these factors when deciding when not to cancel a credit card:

- If it’s one of your oldest credit accounts: Length of credit history is important for your credit score. By closing your oldest (or one of your oldest) cards, you risk eventually shortening your average account age. Even though a closed account can stay on your credit report for up to 10 years, once it drops off, you lose that history. Generally, avoid canceling your oldest credit card unless absolutely necessary. Keeping long-term relationships with credit issuers is beneficial.

- If it’s your only card or only card of a type: If you have just one credit card and you cancel it, you’ll have no open revolving credit, which could make it harder to build credit. Or, say, it’s your only card that offers a specific benefit like airport lounge access or a particular purchase protection – ensure you won’t need that benefit. Don’t cancel the only card that provides a unique perk unless you’re sure you’re okay without it.

- If you carry a balance on the card: It’s generally not possible (nor smart) to close a credit card that still has a balance. Issuers usually require you to pay off the balance (or transfer it) before closure. Even if they allow closing with a balance, the credit line disappears which could negatively affect your credit utilization. So, if you’re thinking of canceling, first focus on paying the card in full. Canceling is for accounts at a $0 balance.

- If you haven’t explored alternatives: Sometimes you don’t need to cancel at all – there may be alternatives like downgrading to a no-fee card or getting a retention offer. As a first step, call your issuer and explain your thoughts about canceling. They might offer to reduce your annual fee, give a points bonus to keep you as a customer, or suggest a downgrade option. For example, instead of canceling a card outright, see if you can product change it to something more suitable (as discussed in the previous article about downgrading). Only proceed to cancel if these options don’t pan out or don’t solve your issue.

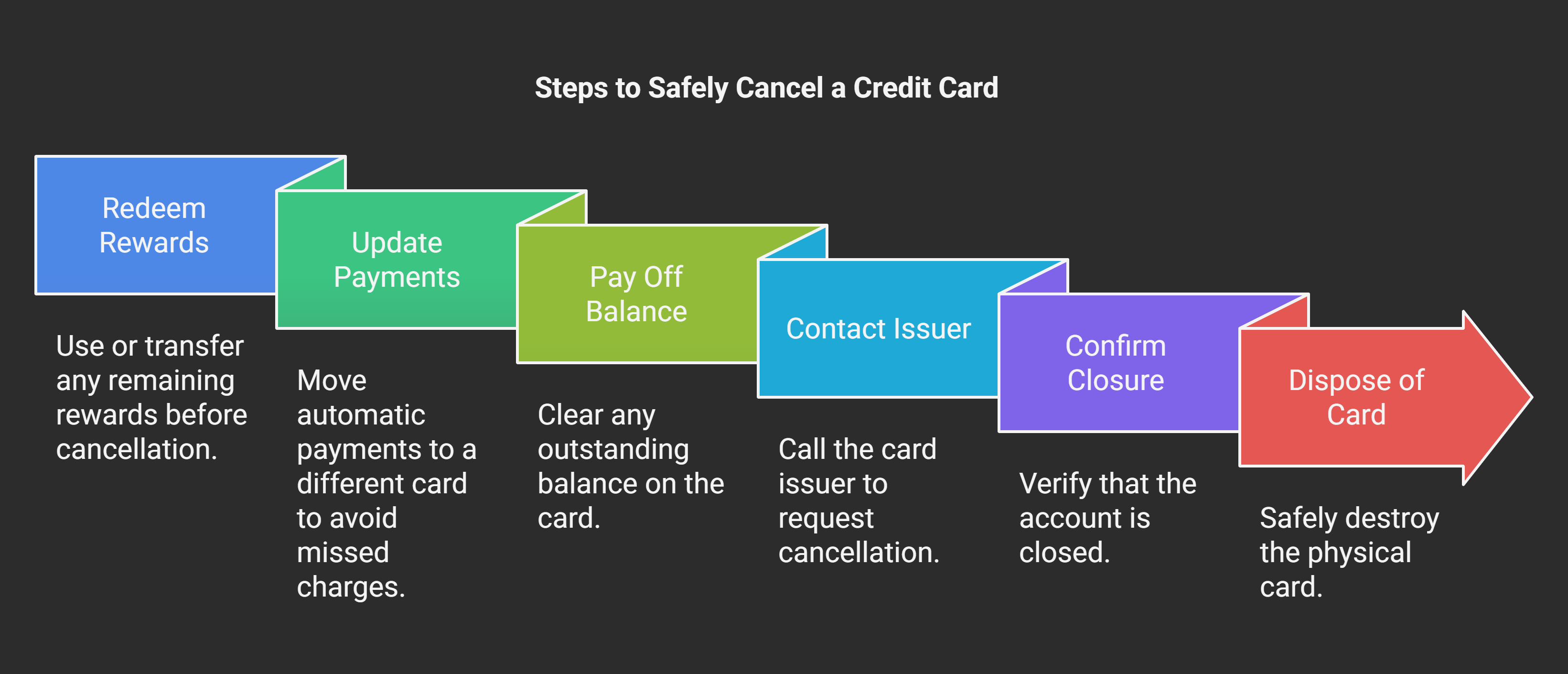

How to Cancel a Credit Card Safely (Step by Step)

If you’ve weighed the reasons and decided that canceling is the right path, follow these steps to do it properly and minimize any negative fallout:

- Redeem any remaining rewards: Before closing, check your card’s rewards balance (points, miles, cash back). Use them up or transfer them if possible. Many issuers state that you forfeit unredeemed rewards when you cancel a card. For instance, if you have a cashback card, redeem the cash back statement credit or direct deposit. If it’s airline miles on a co-branded card, those miles are likely already in your airline’s account (and safe), but if it’s bank points (like Amex Membership Rewards, etc.), make sure you have another active card that earns those or use them, because closing could cause you to lose them. Bottom line: don’t leave value on the table.

- Move or update any automatic payments: Do you have monthly bills or subscriptions charging that card? Before canceling, switch those payments to a different card. Go through recent statements to catch any recurring charges (gym memberships, Netflix, utilities, etc.). Update your payment info with those merchants to avoid failed charges after the card is closed. This ensures a smooth transition so you don’t accidentally miss a bill because it was tied to a canceled account.

- Pay off the card in full: It’s best to have a $0 balance when you cancel. As noted, most issuers won’t let you close until the balance is paid. Even if you could, interest could accrue or you’d still have to manage payments without online access. So pay off any outstanding balance and pending charges. If you can’t pay it all off, you might consider a balance transfer to move the debt to another card (preferably one with 0% interest) before canceling. That way, the account you want to close is cleared.

- Contact your credit card issuer to cancel: Call the customer service number on the back of your card and let them know you’d like to close your account. This is often handled by a retention specialist who may ask why and possibly offer incentives to stay. If your mind is made up, politely decline and confirm you want to proceed with cancellation. During this call, confirm that your balance is zero and that any scheduled payments or fees are resolved. Also ask whether you will receive a confirmation of the account closure (some send an email or letter). Make a note of the date and time of the call and the representative’s name for your records.

- Confirm the account is closed: After a few days, log in to your online banking or call back to ensure the account status shows as “closed.” You can also check your credit report after a month or so to see that it’s reported as closed at customer’s request (which is the ideal notation). Keep an eye out for any trailing charges or refunds: Sometimes merchants might issue a refund to your card after it’s closed or a subscription you forgot about tries to charge. Most issuers will still process those (for example, a refund might show up and you’d need to call to get a check mailed, or a charge will be rejected). It’s a good idea to watch the account for a couple of billing cycles.

- Safely dispose of the card: Once closed, destroy the physical card (and any duplicates, like an authorized user’s card) for security. Cutting it up or shredding it ensures no one can use the card number. Also delete any saved card information from online retailers to avoid confusion or attempted charges.

By following these steps, you’ll have canceled your credit card cleanly, with minimal loose ends.

How Canceling a Card Affects Your Credit (and How to Lessen the Impact)

One of the biggest concerns with canceling a credit card is how it might affect your credit score. Here’s what to expect and tips to soften the impact:

- Credit utilization: This factor is the immediate way canceling can hurt. Your credit utilization is the percentage of available credit you’re using. When you close a card, you lose that card’s credit limit, potentially making your total available credit smaller. If you carry balances on other cards, your utilization ratio will jump up. For example, say you have two cards each with a $5,000 limit ($10,000 total). You usually carry about $2,000 in combined balance (20% utilization). If you cancel one card, your available credit drops to $5,000 total, and now $2,000 is 40% utilization – a significant increase that could lower your score. How to mitigate: Before canceling, try to pay down balances on other cards to keep your utilization low. If possible, aim to use less than 30% of your remaining total credit (the lower, the better).

- Length of credit history: Canceling a card does not immediately erase its history. Closed accounts in good standing can stay on your credit report for up to 10 years, continuing to count toward your length of history during that time. So in the short term, your average age of accounts doesn’t change. However, going forward, that card will eventually drop off and no longer age, and new accounts you open will bring averages down. Additionally, credit scoring models consider the average age of open accounts too – by closing one, you may slightly alter that metric.

- Mix of credit: Having open revolving credit (like credit cards) is good for your credit mix. If you cancel your only credit card, your mix might be less optimal (you’d have only installment loans or no revolving credit). Most folks have multiple cards, so closing one won’t change the mix category from the scoring perspective (you still have other cards). But if it leaves you with zero credit cards, expect a bit of a hit due to lost mix. Mitigation: Make sure you keep at least one card open for credit mix and ongoing positive history (even if it’s just a no-fee card you use occasionally).

- Hard inquiries: Canceling a card does not create a hard inquiry – you’re not applying for credit, just closing an existing line. However, if you plan to get a new card to replace it, that new application will cause an inquiry. Just factor that into your overall credit planning.

- Overall impact: If you have a solid credit history and low balances, canceling one card might only have a small temporary impact on your score. If your credit history is shorter or you carry debt, the impact could be bigger. Generally, folks might see a drop in their credit score after canceling a card mainly due to utilization changes. But if you manage other cards well, your score can rebound over time.

In short, canceling a credit card can cause a dip in your credit score, but it doesn’t have to be devastating. Plan it for a time when you’re not about to seek new credit (like don’t close a card right before applying for a mortgage or car loan). And use the strategies above to minimize any score damage.

Don’t Forget: Maximize the Cards You Keep

Just because you cancel one card doesn’t mean you can’t get great value from your remaining cards. Be sure to make the most of the cards still in your wallet. This is where a tool like Kudos comes in handy. Kudos is a free financial companion that helps you maximize your credit card rewards by tracking hidden perks and suggesting the best card at checkout. (Use code GET20 to get $20 back after your first eligible purchase – a nice bonus when you’re focusing on rewards!).

With Kudos, you can input the cards you still have and it will remind you of benefits you might otherwise forget – like purchase protection, extended warranty, or travel insurance on those cards. Plus, whenever you’re about to make a purchase online, Kudos can recommend which of your cards to use to earn the most rewards or cash back.

This ensures that after canceling the card that wasn’t working for you, you’re fully utilizing the ones you kept. For example, if you canceled a general travel card but kept a gas rewards card and a grocery card, Kudos will prompt you to use the right one for each category to maximize savings.

In essence, cancel the card that no longer serves you, but optimize the heck out of the cards you continue to carry!

FAQs: Canceling Credit Cards

Does canceling a credit card hurt my credit score?

It can, yes – especially in the short term. Canceling a card might increase your credit utilization ratio (if you have balances on other cards) and could eventually reduce your length of credit history. These factors can lead to a lower credit score. However, the impact depends on your overall credit profile. If you have low balances on other cards and a long history, you might see only a small dip.

If you were relying on that card’s credit limit to keep your utilization low, you could see a bigger drop. To minimize harm, pay down other debts first and try to keep older accounts open. Over time, if you manage credit well, your score should recover from a cancellation.

When is the best time to cancel a credit card?

The best time is typically right after you’ve reaped your rewards and just before or after an annual fee posts (if you’re not willing to pay it). For example, if your annual fee posts this month and you’ve decided the card isn’t worth it, you can cancel now – many issuers will refund that fee if you cancel within a month of it posting. Avoid canceling in the middle of a billing cycle if you have ongoing transactions; clear everything first.

Also, do not cancel right before applying for a big loan or new credit – do it when you have a window where a potential credit score dip won’t hurt important financial plans. In essence: after using your rewards and before paying another fee, and when your financial life is otherwise stable.

What happens to my points or miles if I cancel a credit card?

It depends on the type of card:

- For co-branded cards (like an airline or hotel card): generally, any points/miles you’ve already transferred to the airline or hotel’s loyalty program are safe in that external account. Canceling the card won’t make you lose those miles in your airline account. However, if the card has, say, a free hotel night certificate or something, you’d want to use it before canceling because you might forfeit it.

- For bank rewards cards (points or cashback in the issuer’s program): if you cancel and have no other card with that bank’s rewards program, you often forfeit unused rewards. For example, if you cancel the only Citi ThankYou point-earning card you have, any unredeemed ThankYou points are lost. That’s why it’s crucial to redeem or transfer points before canceling. If you have another card earning the same points (like a different card in the same family), your points usually remain intact under that other card/account. Always check the terms or ask a rep what will happen to your rewards upon cancellation to avoid nasty surprises.

Should I cancel a credit card I don’t use?

Not necessarily. If the card has no annual fee and isn’t causing any harm (like temptation to spend), it can actually help your credit to keep it open (it adds to your total available credit and length of history). An unused card isn’t a problem unless you’re concerned about fraud or just truly want to simplify. Some experts actually recommend keeping old no-fee cards open and just using them occasionally to keep them active.

However, if you truly have no use for it and managing it is a hassle, you can cancel – just remember the potential small ding to your credit. A middle ground: you could sock drawer the card (keep it open but not in your wallet) or cut it up so you don’t use it, while still keeping the account active for credit benefits. This way, you don’t have to cancel but you also won’t overspend on it.

Can I cancel a credit card that still has a balance?

Practically speaking, you should pay off the balance first. Most issuers will require the balance to be $0 before processing a cancellation. Even if they don’t, it’s not ideal to cancel with a balance because:

- You’ll still have to pay that card off (the terms of your account agreement still apply until it’s paid, even if you can’t use the card).

- You might lose online access or easy payment options once it’s closed, making it trickier to manage payments.

- There’s a risk of missing a payment if you’re not getting statements as usual, which could hurt your credit badly. In summary, plan to clear the balance either by paying in full or transferring it to another card or loan, then cancel. This ensures a clean break with the card.

Canceling a credit card is a personal decision that should be made with careful consideration. By understanding when it makes sense to cancel and following the right steps, you can confidently close an account that no longer benefits you – while keeping your credit and finances intact. Remember, the goal is to optimize your credit card portfolio for your needs, so don’t be afraid to let go of a card that’s holding you back.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)

.webp)