Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Best Pet Insurance Companies of 2025

July 1, 2025

Top 5 Pet Insurance Companies in 2025

Pets Best – Best Overall 🏆

Pets Best is consistently rated as one of the top pet insurers, excelling in both affordability and coverage flexibility. In fact, Forbes Advisor ranks Pets Best as the best pet insurance company overall in 2025. Among major insurers, Pets Best offered some of the most affordable rates for dog insurance across various U.S. cities. You can choose from three coverage tiers (essential, plus, and elite) and even add wellness packages, making it easy to customize a plan to fit your budget.

Notably, Pets Best has no upper age limit for enrollment and can arrange to pay your vet directly for expensive treatments so you don’t have to front large bills. This combination of low cost, robust coverage options, and convenience makes Pets Best our best overall pick.

Spot – Best for Multi-Pet Discounts

Spot stands out for its comprehensive coverage and perks that benefit households with multiple pets. Spot and many top insurers offer multi-pet discounts around 5–10% for insuring more than one pet, and Spot’s discount is among the highest. Spot’s plans are known for covering many conditions and treatments that some other insurers exclude – from exam fees to alternative therapies and even prescription pet foods.

NerdWallet found Spot had some of the most consistently affordable rates for cat insurance when comparing quotes across providers, making it an excellent choice for cat owners. While Spot doesn’t have a direct-pay option to vets, its wide range of deductibles, reimbursement levels, and unlimited annual coverage option mean you can tailor coverage to your pets’ needs. Overall, Spot’s generous coverage and multi-pet savings make it ideal if you have a menagerie at home.

You can save even more on pet care by using the right credit card for vet bills and pet purchases, since pet owners spend an average of $600-900 annually on their furry friends. Kudos can help you find the perfect cashback or rewards card to maximize returns on pet expenses, giving you a little "treat" every time you pay for Fido's or Fluffy's care!

Lemonade – Best Value (Budget-Friendly)

If price is a primary concern, Lemonade is one of the most affordable pet insurance options on the market. Lemonade’s base accident-and-illness plans come with competitive premiums, and you can customize coverage by adding only the extras you need. In fact, Lemonade offers an impressive array of add-ons – you can elect coverage for exam fees, dental illness, physical therapy, behavioral conditions, end-of-life care, and more.

This modular approach lets you keep costs low while still getting specific protections important to you. Lemonade also provides up to $100,000 in annual coverage (one of the highest limits) with deductible and reimbursement options up to 90%. Do note that many of Lemonade’s best perks are optional add-ons, which will raise your premium slightly. Even so, for many pet parents, Lemonade strikes an ideal balance between low monthly cost and solid coverage.

Embrace – Best for Wellness & Routine Care

Embrace is a top-tier insurer known for comprehensive wellness coverage and plan flexibility. It earned a perfect 5-star rating in NerdWallet’s 2025 analysis. What sets Embrace apart is its focus on preventive care: its optional Wellness Rewards plan has a broader scope than most competitors’ wellness add-ons, covering routine vet visits, vaccines, spay/neuter, dental cleanings and more. Embrace also offers a unique Healthy Pet Deductible benefit that reduces your annual deductible by $50 each year you don’t file a claim, rewarding you for keeping your pet healthy.

Its standard accident/illness policies are highly customizable with multiple deductible and annual limit choices. Embrace even covers some alternative therapies (acupuncture, chiropractic) and behavioral treatment as long as they’re vet-prescribed – great for pet parents seeking holistic care options. With no lifetime limits on payouts and coverage for curable pre-existing conditions after 12 symptom-free months, Embrace provides peace of mind that your pet’s needs (from routine care to serious treatments) are met.

Pumpkin – Best for Comprehensive Coverage

Pumpkin is a newer entrant that has quickly risen to the top rankings thanks to its highly comprehensive coverage. U.S. News & World Report rates Pumpkin as the best pet insurance overall for 2025, and it’s easy to see why. Pumpkin’s standard plan is extremely robust – it includes exam fees, covers illnesses and accidents with a 90% reimbursement rate by default, and has no caps per condition.

There’s also no upper age limit, so even senior pets can enroll. Pumpkin offers an optional Preventive Essentials pack that reimburses a set amount annually for routine care, which can effectively lower your out-of-pocket costs for staying on top of your pet’s health. While Pumpkin’s premiums aren’t the cheapest, the value is in the broad coverage: things like dental illnesses, behavioral issues, and hereditary conditions are covered as long as they aren’t pre-existing. For pet owners who want minimal surprises and maximum coverage in a claim, Pumpkin delivers a great package.

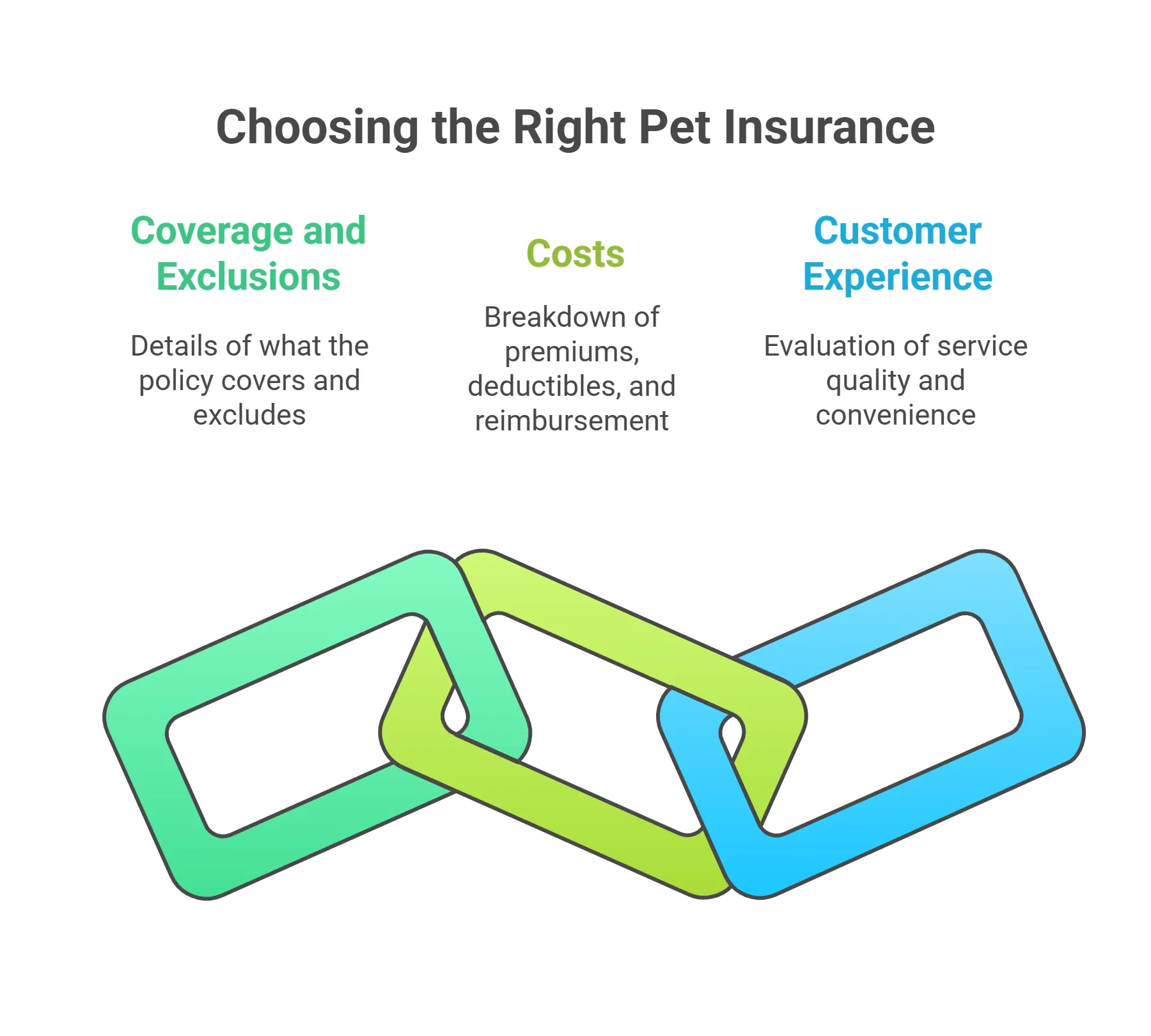

How to Choose the Right Pet Insurance

Picking the best insurance for your pet isn’t one-size-fits-all. Consider the following factors when comparing providers and policies:

Coverage and Exclusions

Look closely at what’s covered by each policy. Virtually all pet insurance covers accidents and new illnesses, including emergencies, surgeries, medications, and chronic conditions. However, coverage details vary – for example, some plans include hereditary or congenital conditions by default, while others might charge extra or have limits. Pay attention to exclusions: pre-existing conditions are never covered, and elective procedures like cosmetic surgeries are also not covered. If you want coverage for routine wellness care (vaccines, dental cleanings, spay/neuter), you’ll need a plan or add-on that specifically includes it – many basic plans do not cover routine care by default.

Also, check if exam fees, alternative/holistic therapies, or behavioral treatments are covered; some top insurers (like those we listed) do cover these, whereas others do not. The goal is to match the policy’s coverage with your pet’s needs – for instance, if you have a breed prone to dental issues or hip dysplasia, ensure the policy doesn’t exclude those treatments.

Costs: Premiums, Deductibles and Reimbursement

Budget is a big factor. Pet insurance has three main cost levers: the premium, the deductible, and the reimbursement percentage. You’ll want to strike a balance between an affordable premium and a deductible you could manage in an emergency. A higher deductible will lower your premium, but means you pay more out of pocket when using the insurance. Conversely, a low deductible and 90% reimbursement sounds great at claim time, but comes with a higher premium. Compare quotes from a few top companies for your pet’s age and breed – premiums can vary widely.

Also consider any annual coverage limit: some budget plans cap payouts, which keeps premiums down, while others offer unlimited coverage. If you can swing it, a plan with a high limit or no cap is ideal for peace of mind, but a lower cap plan can be a reasonable trade-off to save money on premiums. Pro tip: get your pet insured while they’re young and healthy – premiums rise with age, and enrolling early means fewer pre-existing issues that won’t be covered later.

Customer Experience and Waiting Periods

Insurance is only as good as its performance when you need it, so consider the insurer’s reputation and service. Look for reviews or ratings on claim approval speed and customer satisfaction. The top providers we chose generally have above-average reviews for paying claims promptly and easy mobile/apps for filing claims. Also, take note of waiting periods – all policies impose a waiting period after you enroll before coverage kicks in.

Some companies have longer wait times for specific issues like orthopedic conditions. While waiting periods are a one-time inconvenience, an insurer with an excessively long or complicated waiting period policy could be frustrating if your pet needs care soon after signup. Finally, evaluate extras that enhance the experience: does the insurer offer a 24/7 vet helpline for advice? A mobile app for claims? Direct pay to vets? These can add convenience. In short, when choosing, weigh the coverage and cost against these service factors to find the best overall value for you and your pet.

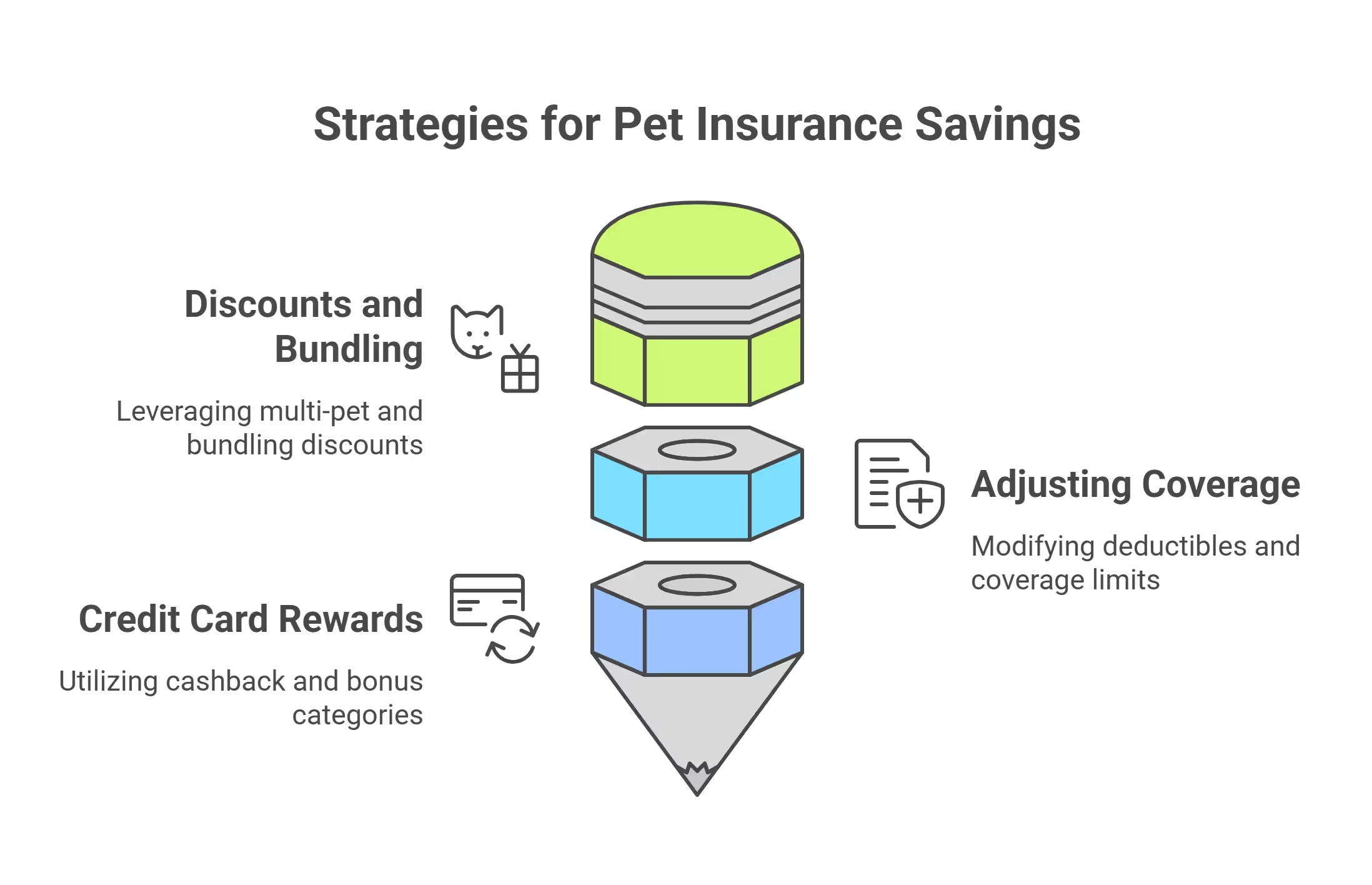

Tips to Save Money on Pet Insurance

Pet insurance provides financial protection, but you can also employ these strategies to keep costs down:

Leverage Discounts and Bundling

Many insurers offer discounts that you should take advantage of. The most common is a multi-pet discount – as discussed, insuring additional pets with the same provider can knock 5–10% off your premiums. If you have more than one furry friend, putting them on the same policy could yield significant savings. Some companies also give a discount if you pay your premium annually in one lump sum.

Another angle: bundle discounts. Certain insurers that are part of larger insurance groups will discount your pet insurance if you’re also a home/auto customer. For example, Lemonade gives 10% off for bundling pet with a home policy. It’s worth asking about affiliation discounts too – occasionally employers, AAA, military, or other groups have partnerships for reduced pet insurance rates.

Adjust Your Deductible and Coverage to Your Budget

You can control your pet insurance cost by tweaking the policy parameters. If premiums are feeling high, consider choosing a higher deductible or a lower reimbursement percentage. For instance, moving from a $200 to a $500 deductible, or from 90% to 70% reimbursement, can significantly cut your monthly premium. Just be sure you could afford that higher out-of-pocket share if an emergency does occur. Similarly, if your plan has an option to select an annual payout limit, you might opt for a slightly lower limit to save on premium, provided it would still cover the vast majority of potential vet bills.

Keep an eye on promotions: some insurers occasionally offer sign-up incentives like gift cards or discount months. And always comparison shop between a few of the best companies – rates can differ for the same pet. Once you have insurance, reassess at renewal; if your premium jumps, it might be worth getting new quotes. Adjusting coverage is a fine balancing act, but it can help you land a premium that doesn’t break the bank while still protecting against major costs.

Use Credit Card Rewards on Pet Expenses

Even with pet insurance, you will have routine out-of-pocket costs – and one often-overlooked way to save on those is by using a rewards credit card. As noted, pet owners spend hundreds each year on food, supplies, and vet visits. By putting these purchases on a cashback or points card, you effectively get a discount or kickback. For example, a 2% cashback card turns a $800 emergency vet bill into $16 back in your pocket – not huge, but every bit helps.

Some credit cards have bonus categories that can apply to pet spending: a card that gives extra points at supermarkets will reward you for buying pet food at the grocery store; some cards occasionally feature pet stores or vet offices in rotating 5% cashback categories. A few new card products even come with pet-related perks or insurance – for instance, one specialty card was offering up to $10,000 in pet insurance coverage as a benefit. At minimum, using a card to pay your vet can defer the payment or allow you to finance big expenses at 0% interest if you have a promotional offer.

Tip: The free Kudos tool can automatically recommend the credit card from your wallet that will earn the most rewards for a given purchase, ensuring you never miss out on savings when paying for pet care. Over a year, these little rewards can add up to a nice chunk of change back – essentially a rebate on the money you’re spending to keep your beloved pet healthy.

Frequently Asked Questions about Pet Insurance

Is pet insurance worth it in 2025?

Yes, pet insurance can be worth it if you might struggle to pay a large unexpected vet bill out-of-pocket. Veterinary care costs have been rising – for example, an emergency vet visit can average $800–$1,500, and complex surgeries can exceed $5,000. Paying a moderate monthly premium for insurance can save you from difficult financial decisions when facing those big bills.

Does pet insurance cover pre-existing conditions?

No, pet insurance generally does not cover pre-existing conditions. A pre-existing condition is any illness or injury your pet showed signs of before your policy’s effective start date. All major pet insurers exclude these conditions – meaning if your dog was diagnosed with diabetes before you bought a policy, that condition (and related treatments) would typically not be reimbursed.

Does pet insurance cover routine care like vaccinations and checkups?

No, not under a standard accident/illness policy. Routine and preventive care is not covered by default in most pet insurance plans. Pet insurance is designed mainly for unexpected injuries and illnesses. That said, many insurers offer optional wellness plans or add-ons that do cover routine care. For example, Embrace’s Wellness Rewards or ASPCA’s Preventative Care add-on will reimburse a set amount for things like shots, dental cleanings, and wellness visits. These add-ons work more like prepaid savings plans – you pay extra premium and get an allotted budget for routine services. Whether it’s worth adding a wellness plan depends on your needs; some pet owners prefer to just budget for routine care themselves.

Can I use any veterinarian with pet insurance?

Yes, with most pet insurance you can visit any licensed veterinarian of your choice. Pet insurance doesn’t have “network providers” like human health insurance does. You typically pay your vet upfront and then submit a claim to your insurer, who reimburses you. This means you’re free to use any licensed vet, emergency clinic, or specialist in the U.S.

Will pet insurance pay my vet directly?

Yes, in some cases. A few pet insurance companies offer direct vet pay options, but it’s not yet common. The norm is you pay the vet, then get reimbursed. However, Trupanion pioneered a system where they can pay the vet at checkout for covered charges – they have software integrated with many clinics that lets claims be processed immediately so you only pay your portion of the bill. Pets Best also can arrange direct payment to vets for large expenses with prior approval. If direct pay is important to you, check if your vet is able to work with these insurers’ systems. For most other companies, you’ll need to file a claim and wait for reimbursement by check or direct deposit.

Conclusion: Protecting Your Pet & Your Wallet

In 2025, there are more quality pet insurance choices than ever – which is great news for pet parents seeking financial security. The best pet insurance companies can reimburse 70–90% of costly vet bills, enabling you to say “yes” to care your cat or dog needs without dreading the credit card debt. Whether you prioritize the cheapest premium, the broadest coverage, or extra perks like wellness coverage or direct vet pay, there’s a plan out there for you. Take some time to compare quotes from a few of our top picks, read the fine print on coverage details, and consider your pet’s specific risks.

Most importantly, don’t wait until your pet is older or has health issues – by then, insurance may not cover what you need. Getting insured while your pet is healthy is the key to unlocking full protection. And if the process feels overwhelming, remember you can adjust as you go.

Finally, as you’re optimizing your pet’s health coverage, why not optimize how you pay for it? Using a tool like Kudos can ensure you’re getting the maximum cashback or points when you pay those vet bills or buy pet food, adding a little extra savings on top of what insurance will reimburse. It’s like a treat for your wallet every time you treat your pet!

Supercharge Your Credit Cards

Experience smarter spending with Kudos and unlock more from your credit cards. Earn $20.00 when you sign up for Kudos with "GET20" and make an eligible Kudos Boost purchase.

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)