Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

First Latitude Assent Mastercard® Secured Credit Card Review: No Fee Secured Card That Rewards Your Payments

July 1, 2025

The First Latitude Assent Mastercard® Secured Credit Card is a unique secured credit card designed for people building or repairing their credit. It charges no annual fee and even rewards you with 1% cash back for making on-time payments – a rare perk for a card aimed at those with bad or no credit.

Backed by Synovus Bank, this card requires a refundable security deposit (starting at $200) which becomes your credit line. Below, we break down the key features, pros and cons, and how to use the First Latitude Assent card to boost your credit score.

Key Features of the First Latitude Assent Card

No Annual Fee, But Watch the APR

One of the biggest selling points of the Assent card is its $0 annual fee. You won’t have to pay just to hold this card, which is great news if you’re on a tight budget. In contrast, its sister card charges a $29 yearly fee. The trade-off? The Assent card carries a higher interest rate – a 28.24% variable APR on purchases. This APR is on the high side, so you’ll want to avoid carrying a balance if possible. Luckily, if you pay your statement in full each month, you can completely avoid paying any interest. The key is to use the card for small purchases and pay them off promptly – that way the high APR won’t matter.

Refundable Security Deposit = Your Credit Line

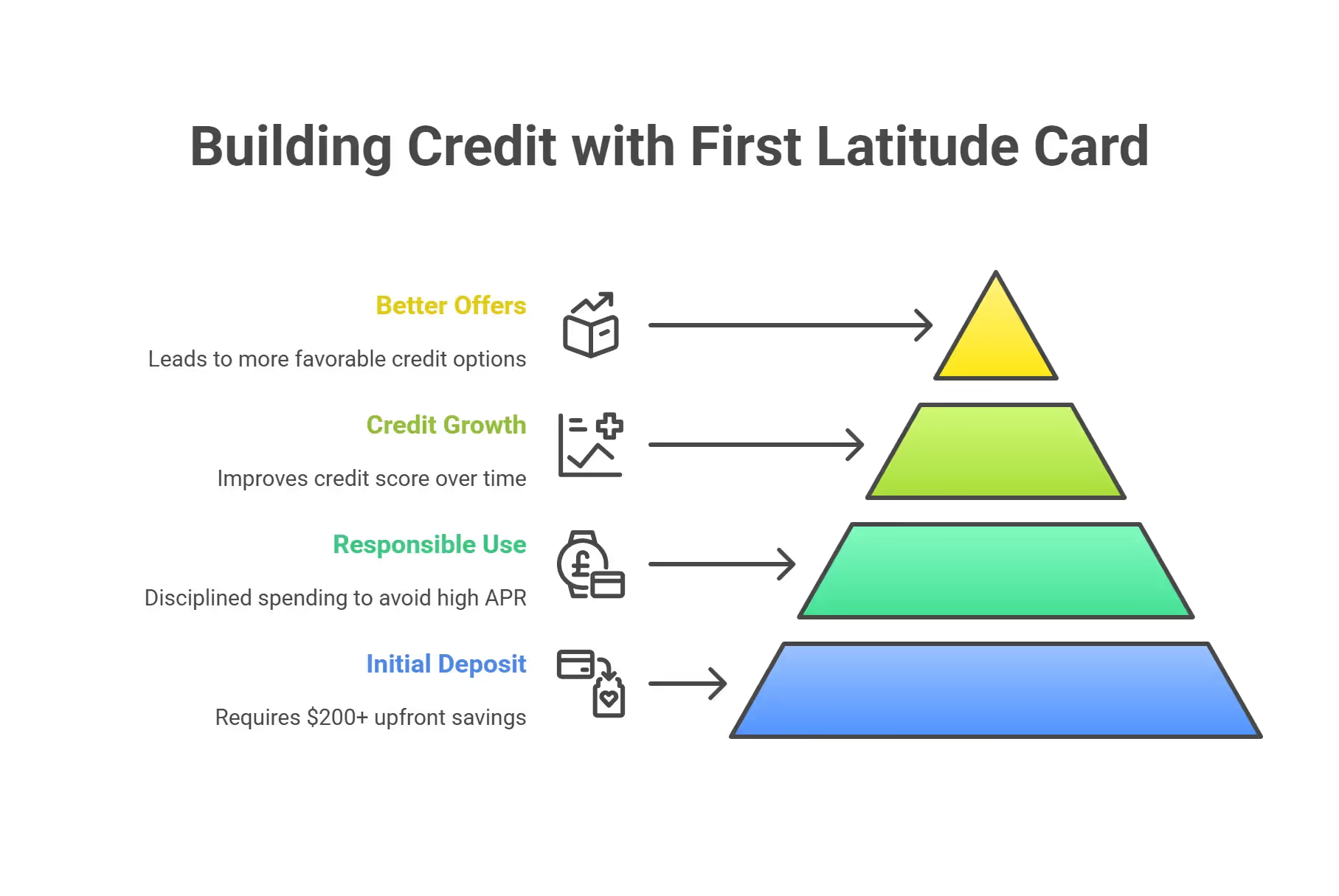

Like all secured credit cards, the First Latitude Assent requires a security deposit to open an account. You’ll need to put down at least $200, and whatever amount you deposit becomes your initial credit limit. First Latitude adds a quirky requirement – when you’re ready to close the card and get your deposit back, you must send your physical card back by mail to the issuer. So don’t throw the card away if you decide to cancel; mail it in to reclaim your money. Also, unlike some competing secured cards, the Assent version currently expects the full deposit upfront. Plan to have your $200 ready when you apply so you can activate your card without delay.

Credit Reporting and Builder-Friendly Features

First Latitude delivers on credit building by reporting to all three major credit bureaus – Equifax, Experian, and TransUnion. The Assent card requires no prior credit score for approval, just age 18+, no active bankruptcy, and identity verification. With no hard credit pull, approval odds are high. Once approved, make small charges and pay on time to see credit score increases. Key tips: pay in full, stay under 30% utilization, and never pay late. The card's monthly reporting will gradually build your credit.

Pros and Cons (Is It Worth It?)

Pros of First Latitude Assent

- No Annual Fee: You won’t pay a yearly maintenance fee, which is relatively rare among “credit-builder” cards. Many competitors charge $25-$35/year just to have the card, so Assent’s $0 fee is a wallet-friendly advantage.

- Easy Approval, No Credit Needed: There’s no minimum credit score required. Even if you’re just starting out or rebuilding from past issues, you can likely get approved as long as you meet basic criteria. Plus, the application won’t ding your credit score since it’s a soft pull. This makes it a low-risk way to start building credit.

- 1% Cash Back on Payments: Perhaps the most unique perk – you actually earn 1% back when you pay your bill. Essentially, for every $100 you pay toward your card balance, you get $1 in rewards. This is a nice incentive to pay on time and more than the minimum. Those rewards accrue as points which you can redeem as statement credits. While 1% isn’t a huge amount, it’s free money for good behavior – a rarity, since most secured cards offer no rewards at all. Over time, this could offset small fees.

Cons of First Latitude Assent

- High APR (Don’t Carry a Balance): With a 28.24% variable APR, interest charges can be steep if you don’t pay off what you charge. For context, this rate is higher than a typical prime credit card. While building credit, it’s best to only charge what you can pay off monthly. That way, you avoid interest entirely. If you anticipate needing to carry a balance, a lower-APR secured card might save you money despite any annual fee.

- Security Deposit Required: As with all secured cards, you must tie up a chunk of money as a deposit. The minimum $200 could be a hurdle for some. If you can’t spare that, you won’t get approved. The deposit is refundable eventually, but only when you close the account. So your cash is locked in the meantime.

- Limited Credit Line & No Upgrade Path: Your credit limit equals what you deposit, and maximum is $2,000. There’s no indication that First Latitude will increase your limit without additional deposit or “graduate” you to an unsecured card. Some issuers may bump you up or return your deposit after 6-12 months of good behavior – First Latitude doesn’t advertise such a program. You might eventually need to apply for a different card to continue growing. Until then, keep your utilization low to get the most credit score benefit.

Comparing First Latitude Assent Mastercard® Secured Credit Card with Other Credit Cards

When considering the Comparing First Latitude Assent Mastercard® Secured Credit Card, it's helpful to compare it with other popular options in the credit builder card category:

- Annual fee: $0

- Security deposit: Flexible, based on the amount transferred to Credit Builder account

- Key features: No credit check to apply, reports to all three major credit bureaus

- Standout feature: No minimum security deposit required

Capital One Quicksilver Secured Cash Rewards Credit Card:

- Annual fee: $0

- Security deposit: Minimum $200, which becomes your credit limit

- Key features: 1.5% cash back on most purchases, automatic credit line reviews

- Standout feature: Earn rewards while building credit

Current Build Visa® Credit Card:

- Annual fee: $0

- Security deposit: Flexible, based on the amount transferred to Build account

- Key features: No credit check required, reports to all three major credit bureaus

- Standout feature: Linked to Current banking app for easy fund transfers

Each card offers unique benefits tailored to different spending habits and preferences. Consider your personal financial goals when choosing the best card for you.

Key Takeaways:

- First Latitude Assent Mastercard® Secured Credit Card with Other Credit Cards excels in helping people build credit

- Chime Card™ offers flexibility with no minimum deposit

- Capital One Quicksilver Secured provides cash back rewards

- Current Build integrates with banking app for convenient use

[[ CARD_LIST * {"ids": ["3069","3058", "5132"]} ]]

How to Apply and Build Credit with First Latitude

Application Process (Soft Pull & Requirements)

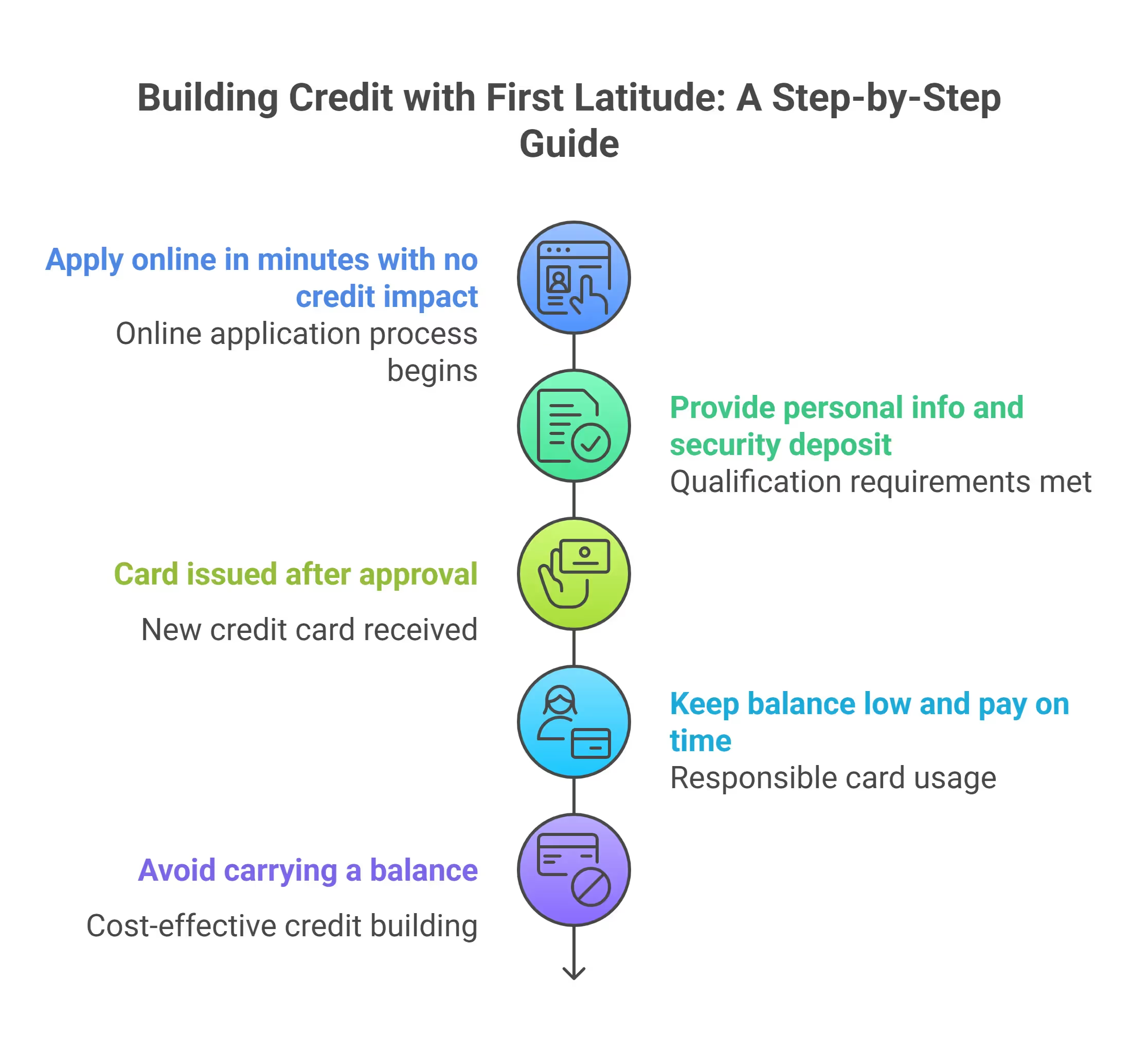

Applying for the First Latitude Assent Mastercard is straightforward – you can apply online in a few minutes. Uniquely, you can do so with “no impact” to your credit score. This is great if you’re worried about hurting your score with a hard credit check. To qualify, you should be age 18 or older, a U.S. resident, and not currently in bankruptcy. You’ll need to provide personal info and at least the $200 security deposit. Once approved, you fund your deposit, and your card will be issued.

Using the Card Responsibly (Credit-Building Tips)

After you receive your shiny new First Latitude card, focus on responsible usage to achieve your goal: a better credit score. Here’s a game plan:

- Keep Your Balance Low: Since your limit might be small (especially if you only deposited $200-300), try not to max out the card. Aim to use no more than 30% of your credit line at any time. Low utilization benefits your credit score.

- Pay On Time, Every Time: Payment history is the biggest factor in your score. Set up autopay or reminders to never miss a due date. Paying even a day late could incur a fee and be reported as a late payment, hurting your progress. Pay at least the minimum due, but ideally pay in full. Remember, you get 1% cash back on payments – so paying more not only helps your credit, it literally earns you rewards!

- Avoid Carrying a Balance: This card’s high APR means carrying debt is costly. Even though you might be tempted to carry a balance to show activity, it’s not necessary – you can build credit just by using the card and paying it off regularly.

In a few months, if you follow these steps, you should start to see improvement in your credit score. First Latitude reports to all bureaus, so each on-time payment is helping establish your creditworthiness. Many users report being able to move on to an unsecured credit card after ~6-12 months of good history. At that point, you could close the First Latitude card, mail it back and get your deposit refunded – and voila, you’ve graduated! Just be sure to maintain at least one credit account open to keep building your length of credit history.

Conclusion: Is First Latitude Assent Secured Card Right for You?

The First Latitude Assent Mastercard® Secured Credit Card is a friendly option for credit-builders – it’s low-cost, fairly accessible to get, and even gives you a little cash-back reward for paying responsibly. For someone just starting out or rebuilding after credit troubles, it offers a straightforward way to prove yourself financially and grow your credit score.

The high APR means you must be disciplined, and the $200+ deposit means you need some savings upfront. But if you handle it well, this card can be a stepping stone to better credit offers down the road. Kudos can help you take the next step – whether that’s applying for the First Latitude Assent card or comparing it against other top secured cards. With a solid plan and responsible use, you’ll be on your way to a stronger credit profile.

FAQs about First Latitude Assent Mastercard

Does the First Latitude Assent Mastercard® have an annual fee?

No. The Assent Mastercard secured card charges $0 annual fee.

Do I need a good credit score to get this card?

No. No credit score or history is required to be approved for the First Latitude secured cards. It’s designed for people with bad or no credit, so approval is likely as long as you meet the basic requirements and fund the security deposit.

Will applying for First Latitude hurt my credit score?

No. First Latitude’s application uses a soft credit inquiry, which does not impact your credit score. You can apply (or check pre-approval) with confidence that it won’t cause a hard inquiry ding.

Does the First Latitude Assent card report to credit bureaus?

Yes. It reports to all three major credit bureaus (Experian, Equifax, TransUnion) every month. This is crucial for building your credit – consistent on-time payments will be recorded and can help improve your credit score over time.

Can I get my security deposit back from First Latitude?

Yes. Your deposit is fully refundable when you close the account with a zero balance. To get your money back, you’ll need to pay off any balance in full and mail back your physical card to First Latitude. After that, your deposit will be returned to you, typically within a few weeks.

Supercharge Your Credit Cards

Experience smarter spending with Kudos and unlock more from your credit cards. Earn $20.00 when you sign up for Kudos with "GET20" and make an eligible Kudos Boost purchase.

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)