Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

FIT™ Platinum Mastercard® Review (2026) – Fees, Pros & Cons, and Alternatives

July 1, 2025

.webp)

Considering the FIT™ Platinum Mastercard® to rebuild your credit? You’re not alone. This card, issued by the Bank of Missouri and serviced by Continental Finance, is frequently advertised to people with bad or limited credit. It promises an unsecured $400 credit line with no security deposit.

[[ SINGLE_CARD * {"id": "914", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Credit Builders", "headerHint": "Doubled Credit Limit"} ]]

However, is the FIT™ Platinum Mastercard® a smart way to build credit, or will its fees do more harm than good? In this in-depth review, we’ll break down everything you need to know – from fees and features to cardholder experiences – so you can decide if the FIT card is the right fit for you.

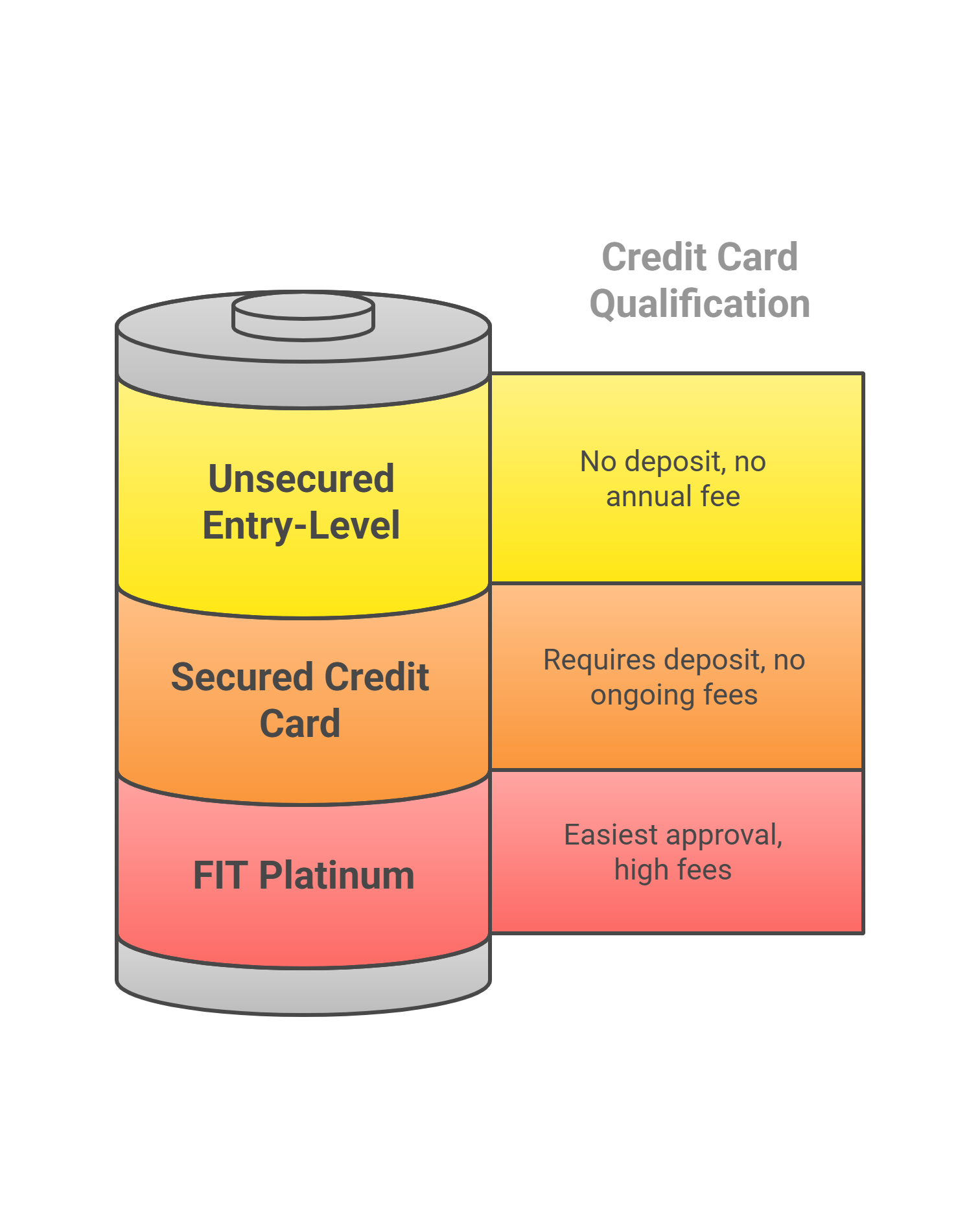

What is the FIT Platinum Mastercard?

The FIT Platinum Mastercard is an unsecured credit card designed for people with poor credit who might not qualify for traditional cards. Because it’s unsecured, you don’t have to put down a security deposit – but that doesn’t mean it’s free. In fact, the FIT card’s defining feature is its cost: it’s loaded with fees. Here’s a quick overview:

- Initial Credit Limit: $400 to start. This is relatively low, and your usable credit will be far less after fees. The card does offer a credit limit increase: if you pay on time for 6 months, your limit can double to $800. While that sounds good, keep in mind you may have paid hundreds in fees by then.

- Purpose: The card’s goal is to help you “rebuild your credit.” It reports to all three major credit bureaus each month, so using it responsibly can improve your credit over time. However, any card that reports to bureaus can build credit – the FIT isn’t special in this regard, and it comes with significant costs to consider.

Fees and Charges: How Much Does the FIT Card Cost?

Let’s address the biggest drawback upfront: the FIT Platinum Mastercard’s fees are outrageous. Here’s the breakdown:

- One-Time Processing Fee: $95 – This is charged when you open the account. It does not go toward any bill or deposit; it’s just an initial price of admission.

- Annual Fee (Year 1): $99 – Charged to your card upon opening. Immediately, this eats up a quarter of your $400 limit, leaving you with roughly $301 of available credit.

- Monthly Fee (After Year 1): $6.25 per month – Kicks in starting month 13. That’s an additional $75/year in fees on top of the annual fee.

- Annual Fee (Year 2 onward): $125 – Yes, it actually increases in the second year. So in year 2 and beyond, you’ll pay $125 annual plus $75 in monthly fees, totaling $200 in yearly maintenance cost.

- APR: 35.9% (Fixed) – A very high interest rate on purchases. Carrying a balance on this card is extremely expensive.

- Other Fees: Late payment fee up to $40; Cash advance fee: 5% (min $5); Foreign transaction fee: 3%. There’s also a $30 additional card fee if you want an extra card for an authorized user.

In summary, the FIT card could cost you up to $170 in various fees in the first year, and $200+ each year after. These fees do not provide any value in return. They purely make the card issuer money and give you the privilege of carrying the card.

Bottom line: If you take the FIT card, plan for a lot of charges. Always factor these into your budget so you’re not caught by surprise. And if you do get the card, make sure to pay the full balance each month – never carry a balance at 35.9% interest if you can help it.

Trying to build credit without sky-high fees? Consider a no-annual-fee secured card instead. Secured cards require a deposit, but often that’s less money upfront than what you’d pay in FIT’s fees in the first year!

Pros and Cons of the FIT Platinum Mastercard

To be fair, let’s list out where the FIT card actually helps and where it hurts.

Pros:

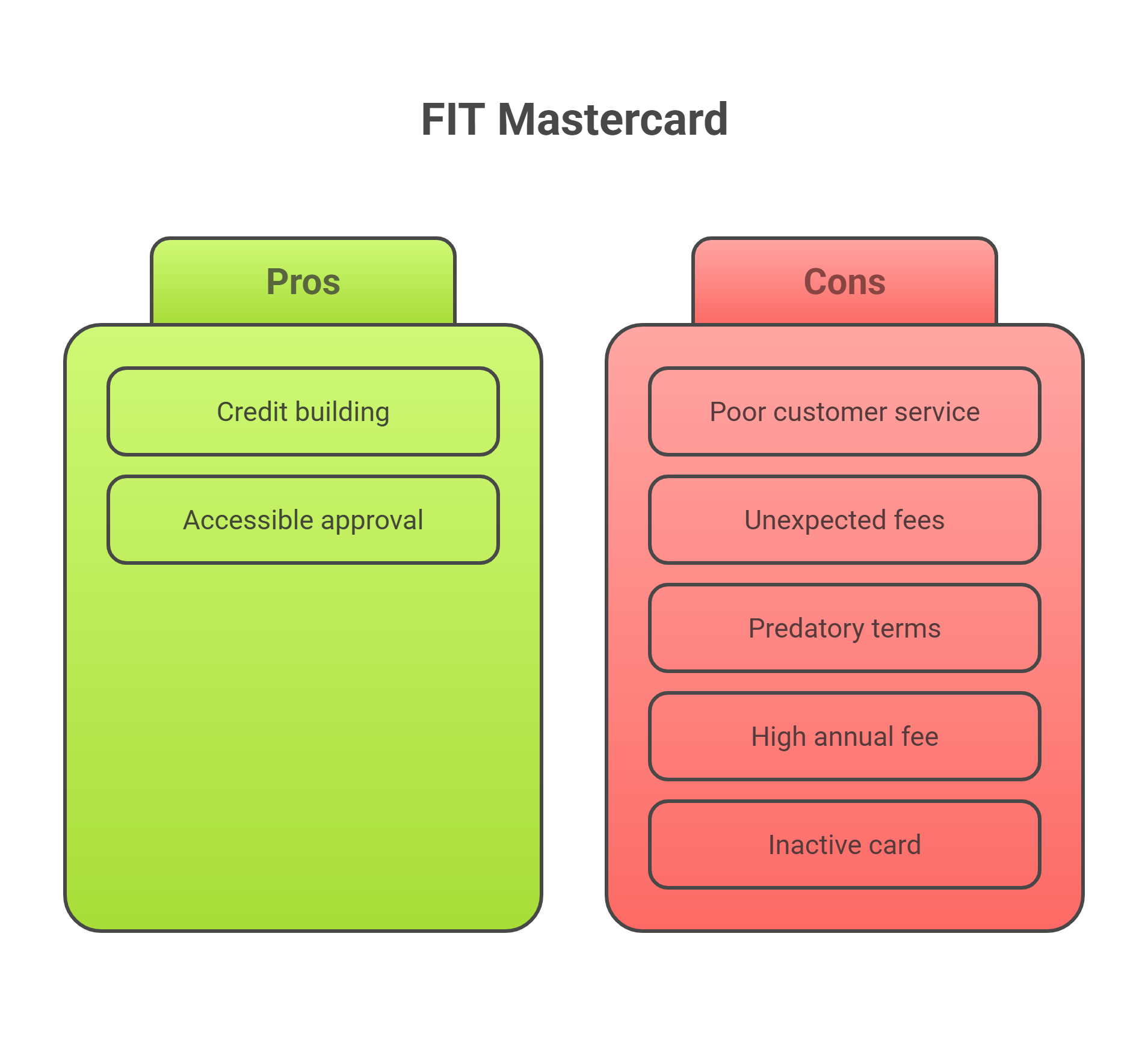

- No Security Deposit Required: Unlike a secured credit card, you don’t have to put down $200-$300 of your own money as collateral. For someone with limited cash, this can be a relief – though remember, the fees you pay essentially add up to a similar amount.

- Lenient Approval: The FIT Mastercard is aimed at people with bad credit or no credit. Even past credit issues or a low score might be approved. There’s no hard credit inquiry to see if you prequalify. In fact, many receive this card as a mail offer with a reservation code, indicating pre-selection.

- Reports to All Bureaus: This is crucial for building credit. The FIT card will report your payment history monthly to Experian, Equifax, and TransUnion. Many “second chance” cards do this, but it’s worth noting: if you use the card responsibly (on-time payments, low balance), it can help improve your credit score over time.

- Credit Limit Increase Opportunity: After 6 months of on-time payments, your $400 limit may increase to $800. This could help your credit utilization ratio slightly.

Cons:

- Extremely High Fees: The array of fees make this card one of the most expensive credit-building options. Over two years you could pay $300+ in fees – money that could have been saved or used as a deposit on a secured card. These fees effectively reduce your available credit and can even lead to a balance on your first statement before you’ve made a single purchase.

- High APR: 35.9% interest means if you carry a balance, finance charges will pile up quickly. For someone trying to rebuild credit, one missed payment or a large carried balance could sink you further. This card must be paid in full monthly to avoid the punitive APR – but the card’s target audience might struggle with that if finances are tight.

- No Rewards or Benefits: Unlike some cards (even some for fair credit) that offer cashback or perks, the FIT Mastercard has no rewards program. There are also no special benefits like travel insurance or purchase protection beyond the basic Mastercard zero liability. You are truly paying fees for the opportunity to hold a bare-bones card.

- No Upgrade Path: This is not a card that graduates to a better product. Some starter cards (e.g., Discover it Secured) will upgrade you to an unsecured card after good behavior. With FIT, once your credit improves, they have no other cards to transition you to. You’ll have to close it or just keep eating the fees until you get a different card.

- Potential for Debt Trap: Because the limit is low and the fees are high, it’s easy to max out this card. For example, after the initial $170 in fees, you’d only have $230 of your $400 limit available. If you spend that, you’re at 100% utilization, which hurts your credit score. Then interest accrues if you don’t pay in full. Many users of cards like this get caught in a cycle of paying just enough to free up a bit of credit, then using it again – all while interest and monthly fees accumulate. It can turn into debt that’s hard to clear despite the small credit line.

Comparing FIT™ Platinum Mastercard® with Other Credit Cards

When considering the FIT™ Platinum Mastercard®, it's helpful to compare it with other popular options in the credit builder card category:

- Annual fee: $0

- Security deposit: Flexible, based on the amount transferred to Credit Builder account

- Key features: No credit check to apply, reports to all three major credit bureaus

- Standout feature: No minimum security deposit required

Capital One Quicksilver Secured Cash Rewards Credit Card:

- Annual fee: $0

- Security deposit: Minimum $200, which becomes your credit limit

- Key features: 1.5% cash back on most purchases, automatic credit line reviews

- Standout feature: Earn rewards while building credit

Current Build Visa® Credit Card:

- Annual fee: $0

- Security deposit: Flexible, based on the amount transferred to Build account

- Key features: No credit check required, reports to all three major credit bureaus

- Standout feature: Linked to Current banking app for easy fund transfers

Each card offers unique benefits tailored to different spending habits and preferences. Consider your personal financial goals when choosing the best card for you.

Key Takeaways:

- FIT™ Platinum Mastercard® excels in customers helping build credit

- Chime Card™ offers flexibility with no minimum deposit

- Capital One Quicksilver Secured provides cash back rewards

- Current Build integrates with banking app for convenient use

[[ CARD_LIST * {"ids": ["3069","3058", "5132"]} ]]

Who Should Consider (or Avoid) This Card?

Ideal Candidate: The FIT Platinum Mastercard might be considered by someone who cannot come up with a security deposit for a secured card but urgently needs a line of credit to start rebuilding credit. For instance, if you need a small credit line to keep your utilization on other cards low, or you want a tradeline on your report and every other option has denied you – FIT could be a last-resort lifeline. Its approval is relatively easy, so it’s an option if you’ve been rejected elsewhere and you’re fully aware of the costs.

However, even in this scenario, you should plan to use the card very sparingly (to keep utilization low) and pay it off every month. Essentially, the only benefit you derive is a positive payment history on your credit report – and nothing else.

Who Should Avoid: Most people looking to build credit will have better options:

- If you have at least $200-$300 for a deposit, a secured credit card will cost far less in the long run. You get your deposit back and pay no ongoing fees.

- If your credit is in the “fair” range, you might actually qualify for an entry-level unsecured card with no annual fee. These have no monthly fees and no upfront program fee.

- Anyone unwilling or unable to handle the strict payment discipline needed for FIT should stay away – missing a payment or maxing the card could make a bad situation worse due to the card’s costs.

Alternatives to the FIT Card: Instead of FIT, consider:

- Secured Credit Cards: These require a refundable deposit but often have zero fees.

- Credit Builder Accounts or Cards: Some fintech companies offer credit-builder loans or cards that help you build payment history without traditional credit card fees or credit checks.

- Other Unsecured Subprime Cards: If you insist on an unsecured card and can’t get a prime issuer’s card, there are a few with slightly less vicious fee structures.

Kudos can help here: By using the Kudos extension or app, you can compare real credit card offers tailored to your credit profile. Instead of jumping on a mail offer like FIT, Kudos might show you alternative credit cards that you pre-qualify for. This way, you don’t end up overpaying for credit-building.

Cardholder Experience and Reputation

It’s important to know what actual users say:

- Customer Service: Continental Finance is known for handling multiple subprime cards. Customer reviews on Trustpilot and Better Business Bureau are generally negative. Common complaints include difficulty reaching customer service, unexpected fees or charges, and issues upon closing accounts. The company does have a BBB rating of A+, but user sentiment is not positive.

- User Reviews: Browsing online forums and review sites, we saw mixed experiences. Some users report that “the card does what it promises” – they were able to get approved with bad credit and by using it lightly and paying on time, they did see their credit score go up. These users accept the fees as the cost of rebuilding credit. However, many others call the card “a scam” or “rip-off.” They feel the fees are predatory; some were upset that the card arrived inactive until they paid the $95 fee, or that their credit line was mostly eaten by the annual fee right away.

- Our take: The FIT Mastercard is legitimate in that it’s a real credit card used by thousands of people, and it can help your credit if handled perfectly. But legitimacy doesn’t equal a good deal. The harsh terms make for a very narrow usefulness. Essentially, the card is taxing the desperate – it’s offered to those with few choices, and if you accept it, you pay dearly for the service of credit access.

FAQs about the FIT Platinum Mastercard

Is the FIT Platinum Mastercard legit or a scam?

The FIT card is a legitimate credit card – it’s issued by the Bank of Missouri and managed by Continental Finance. It will arrive with the Mastercard logo and can be used anywhere Mastercard is accepted. However, many people label it a “scam” because of its business model: the fees are so high that it feels like you’re being cheated. Rest assured, if you apply and follow the terms, you will get a real card and it can help your credit.

How do I apply for the FIT Mastercard?

You can apply online via the official website. The application does not require a hard credit pull for the initial decision – you’ll get an answer quickly. If approved, you must pay the $95 processing fee before they send out the physical card. Be prepared to cover that fee immediately. Once you pay it, your card arrives and you can activate it.

Can I increase my credit limit on the FIT card?

Initially, your credit limit is $400. The only way to increase it is by demonstrating responsible use. After 6 months of on-time payments, FIT may automatically double your limit to $800. There is no additional fee for this increase. Keep in mind: $800 is still a low limit, so continue to keep your balances low. Also, the increase isn’t guaranteed if you’ve had any late payments or returned payments. Beyond this one-time bump, there generally aren’t further increases advertised for the FIT card. If your credit improves significantly, a better strategy is to apply for a new card with a higher limit and lower fees, then consider closing the FIT card if it no longer provides value.

What happens if I max out the card or miss a payment?

If you max out the $400 limit (not hard to do, considering the fees take up a lot of it), two things happen: your credit score could suffer due to 100% credit utilization, and you’ll need to pay it down before using the card again. If you miss a payment, you’ll be hit with a late fee, and it will be reported to the credit bureaus as a missed payment, damaging your credit score.

Should I keep the card after my credit improves?

Probably not. Once you’ve achieved a better credit score, you’ll likely qualify for credit cards with far fewer fees and maybe even rewards. At that point, the FIT card’s fees become an unnecessary burden. There’s no benefit like cashback or travel points keeping you there. Many cardholders choose to close the account after a year or two once they can get approved elsewhere. If you do so, try to have another credit line already open (to soften any credit score impact from closing one).

Does the FIT Platinum Mastercard offer any rewards or perks?

No, the FIT card has no rewards program. You won’t earn cash back, points, or miles on any purchases. It also doesn’t come with introductory APR deals or balance transfers. The only “perks” are the standard Mastercard benefits like zero fraud liability. In short, this card’s sole function is to provide a line of credit for credit-building. If you’re looking for rewards, you’ll need to look at other cards.

Final Verdict

The FIT™ Platinum Mastercard® is a tool of last resort. Yes, it can help build or rebuild your credit if you have no other options – it reports to all bureaus and has lenient approval. But it does so at a very steep price. For most people, the same credit-building progress can be achieved with far fewer fees (and headaches) by using alternative products like secured cards or other entry-level cards.

Before accepting the FIT card, make sure you’ve explored all alternatives. And if you do get the card, use it cautiously: charge a small amount periodically, pay it off in full, and reevaluate after 6-12 months. You want to graduate to better credit products as soon as you responsibly can, so that you’re not paying $170+ each year for the privilege of carrying a subprime credit card.

Kudos is here to help. As your free credit card assistant, Kudos can guide you to better card choices as your credit improves, and help you stay on top of payments for any card you use. Rebuilding credit is a journey – with the right strategy, you’ll reach your destination faster and cheaper. Good luck on your credit-building journey!

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)