Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

State Farm® Premier Cash Rewards Visa Signature® - Review & Key Benefits

February 6, 2025

Key Features of the State Farm Premier Cash Rewards Visa

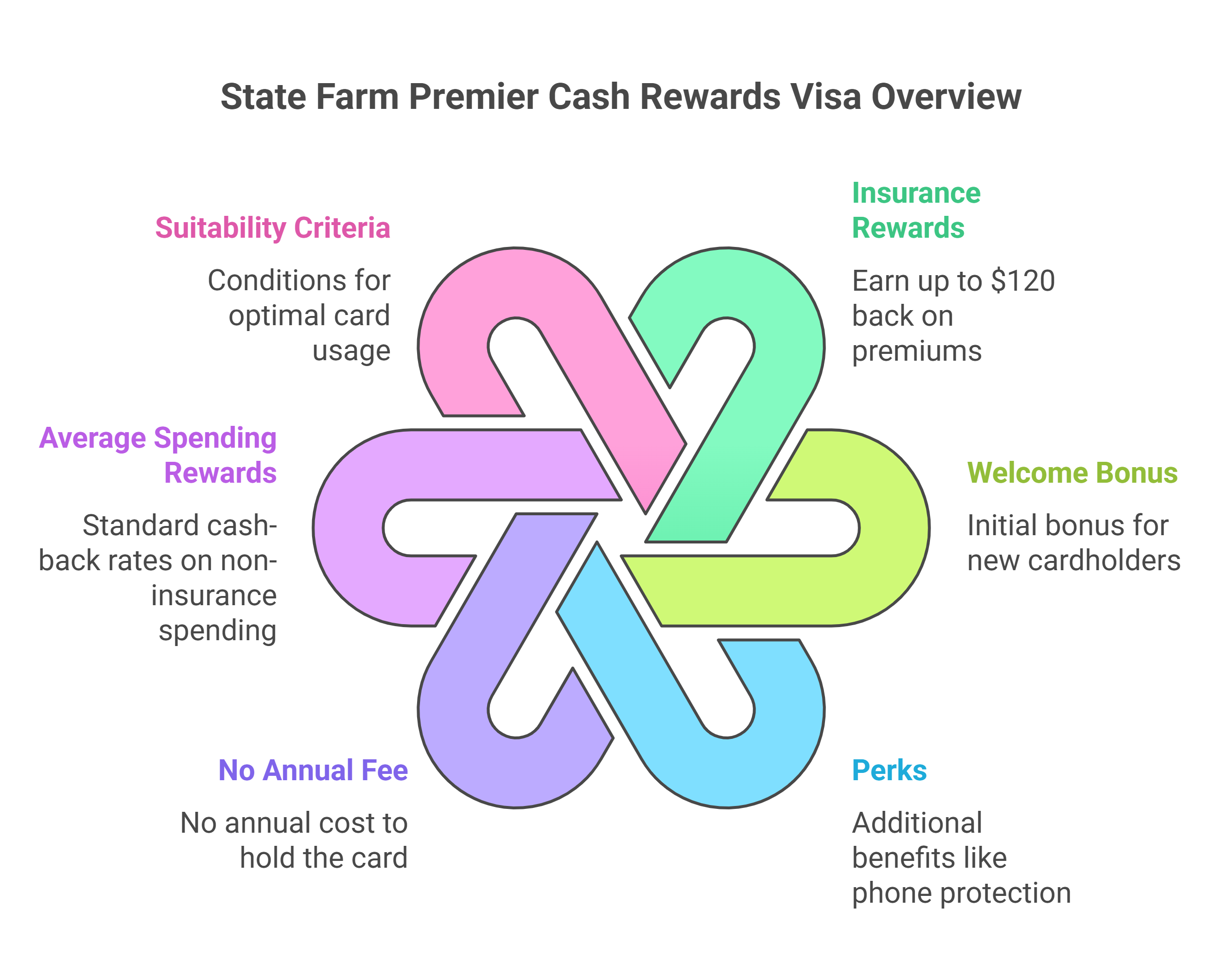

The State Farm® Premier Cash Rewards Visa Signature® is a co-branded rewards card issued by U.S. Bank for State Farm customers. It offers bonus cash back on insurance payments and other everyday categories, with no annual fee.

[[ SINGLE_CARD * {"id": "2205", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Cash Back Seekers", "headerHint": "$150 Cash Back"} ]]

Rewards

The Premier Cash Rewards Visa Signature® earns 3% cash back on insurance premium payments up to $4,000 per year, 2% cash back at gas stations, EV charging stations, drugstores, grocery stores, and on dining, and 1% on all other purchases. In practical terms, 3% back on insurance is a unique perk – insurance is a rare rewards category on credit cards. However, note the 3% is capped at $4k of insurance spend per year. Even if you max out that cap, that’s $120 back on $4,000 of insurance.

Bonus Offer

New cardholders can earn a $150 cash back bonus by spending $500 within the first 90 days of account opening. This is a straightforward sign-up bonus with a low spending requirement, making it fairly easy to attain. The $150 will typically be credited to your rewards balance within a couple months of meeting the spend.

Fees

There is no annual fee for this card. This means any rewards you earn are net gains, as you’re not paying to hold the card. Keep in mind, though, foreign transaction fees apply – a 3% fee on purchases made outside the U.S.. In other words, this is not the ideal card to use abroad due to that surcharge. Also, the regular APR will vary with your credit (there’s no special 0% intro APR on this rewards card, unlike its sibling “Good Neighbor” card).

Eligibility

You will generally need to be a State Farm customer to get approved for this credit card. Applications ask for a State Farm account number or insurance policy number. Additionally, because it’s a Visa Signature card, you’ll likely need good to excellent credit for approval. If you’re not already with State Farm, this card isn’t meant to entice you to switch insurers – it’s more of a perk for existing customers.

Pros and Cons of the State Farm Rewards Visa Card

Under the hood, the State Farm Premier Cash Rewards card is a U.S. Bank-issued cash-back card with a few standout features – and a few drawbacks. Let’s break them down:

Pros

- 3% Back on Insurance: If you’re paying hefty insurance premiums to State Farm, getting 3% back is a nice perk. For a loyal State Farm client, this essentially acts like an automatic small discount on your insurance bill. No other mainstream card consistently offers 3% on insurance payments year-round, so this is the major selling point of the card.

- 2% on Useful Categories: The 2% cash back at gas stations, grocery stores, drugstores, dining, and EV charging covers a lot of everyday spending. Earning 2% in these categories is decent – it’s on par with many other cash-back cards’ category rewards. This means the card isn’t a one-trick pony; you can use it for dinner, fill-ups, and pharmacy runs and still get a solid 2% back, in addition to using it for insurance bills.

- No Annual Fee & Easy Bonus: The card costs nothing to carry, so you don’t have to worry about “earning back” an annual fee each year. The one-time $150 bonus for a low $500 spend is also very accessible – essentially a 30% rebate on your first $500 of purchases. A nice extra if you were going to spend that money anyway in 3 months.

- Extra Cardholder Perks: As a Visa Signature card, it comes with some valuable protections. Notably, cell phone protection is included – if you pay your monthly cell phone bill with the card, your phone is insured against damage or theft. This is a significant perk that could save you money. Additionally, there’s an auto insurance deductible reimbursement benefit: if you have a State Farm auto policy and you use this card for at least 8 purchases in the month before an accident, you can get up to $200 of your auto insurance deductible reimbursed. These “good neighbor” perks reward you for using the card regularly and tie into State Farm’s insurance products. The card also includes standard Visa Signature benefits like purchase security and extended warranty coverage.

Cons

- State Farm Customers Only: This card is not available to the general public in the way most credit cards are. You have to be a State Farm customer to even apply. That makes its potential user base limited. If you’re not with State Farm for insurance or banking, there’s no practical way to get this card – and no strong reason to become a customer just for the card, given its fairly average rewards outside the insurance category.

- Mediocre Rewards Outside Insurance: Beyond the unique insurance rebate, the rewards are underwhelming compared to market leaders. 2% back on gas/groceries/dining is good, but note that’s a limited list – many top cash-back cards offer 2% on all purchases or higher rotating category rewards. And 1% on “everything else” is just baseline.

- Foreign Transaction Fee: As mentioned, this card charges a 3% fee on transactions made outside the U.S.. That immediately makes it a bad choice for traveling abroad or even for online purchases from international merchants. Many no-annual-fee cards these days waive foreign transaction fees, so this is a notable downside if travel is on your agenda.

- No 0% APR Intro (for this card): Premier Cash Rewards card does not offer an introductory 0% APR period on purchases or balance transfers. If you were hoping to finance a large purchase interest-free, this card won’t help there.

- Reward Redemption is Basic: This isn’t a huge con, but just know that the cash back you earn is not issued as points or miles with fancy redemption options – it’s straightforward cash back. You can redeem as a statement credit, or a deposit into a U.S. Bank checking/savings, or possibly towards State Farm products. There’s no option to transfer points to travel partners or anything exotic.

Comparing State Farm® Premier Cash Rewards Visa Signature® with Other Credit Cards

When considering the State Farm® Premier Cash Rewards Visa Signature®, it's helpful to compare it with other popular options in the cashback credit card category:

- Annual fee: $0

- Sign-up bonus: Cash bonus after meeting spending requirements

- Key rewards: 5% on travel purchased through Chase Travel℠, 3% on dining and drugstores, 1.5% on all other purchases

- Standout feature: Flexible redemption options including cash back, travel, and gift cards

Capital One Savor Cash Rewards Credit Card:

- Annual fee: $0

- Sign-up bonus: Cash bonus after meeting spending requirements

- Key rewards: 3% on dining, entertainment, popular streaming services, and grocery stores

- Standout feature: No foreign transaction fees

Blue Cash Everyday® Card from American Express (rates & fees):

- Annual fee: $0

- Welcome offer: Cash bonus after meeting spending requirements

- Key rewards: 3% at U.S. supermarkets (up to $6,000 per year, then 1%), 3% cash back up to $6,000 per year, then 1%. Cash back is received in the form of Reward Dollars that can be redeemed as a statement credit or at Amazon.com checkout

- Standout feature: This card offers a generous intro of APR on purchases and balance transfers

Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. Eligibility and Benefit level varies by Card. Terms, Conditions, and Limitations Apply. Please visit americanexpress.com/benefitsguide for more details. Underwritten by Amex Assurance Company.

Each card offers unique benefits tailored to different spending habits and preferences. Consider your personal financial goals when choosing the best card for you.

Key Takeaways:

- State Farm® Premier Cash Rewards Visa Signature® with Other Credit Cards excels in giving cash back on incurance payments

- Chase Freedom Unlimited® offers diverse category bonuses

- Capital One Savor Cash Rewards Credit Card rewards dining and entertainment spending

- Blue Cash Everyday® Card from American Express provides strong rewards on everyday purchases

[[ CARD_LIST * {"ids": ["497","3041", "260"]} ]]

Kudos Tip

If you have multiple credit cards, consider using Kudos to optimize your rewards across them. Kudos is a free tool that automatically picks the best card for each purchase to maximize your cashback or points. For example, if you add your State Farm card and another 2% cash-back card to your Kudos wallet, Kudos will suggest using your State Farm Visa for State Farm insurance payments (to snag that 3% back), but it might prompt you to use your 2% card for other purchases where it earns more. This way, you’re always getting the highest reward rate without manually juggling cards.

How to Maximize Rewards with This Card

Pair it with a general cashback card: Because the 3% category is limited and everything else is 1%, many users will get the best value by using the State Farm Premier Cash Rewards card only for insurance and maybe gas/groceries, and using a flat-rate 2% card for all other purchases. For instance, pay your State Farm auto/home insurance with this card to earn 3%, but use a card like Citi Double Cash® Card for bills and shopping to earn 2% instead of 1%. By doing so, you ensure you’re always earning at least 2% on non-insurance spending. This strategy beats putting all spend on the State Farm card just for simplicity, which would dilute your reward rate to a mediocre level.

[[ SINGLE_CARD * {"id": "580", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Frequent Travelers", "headerHint": "Straightforward Rewards"} ]]

Take advantage of the cell phone protection: If you have this card, consider making it your default card for your cell phone bill. Charging your monthly wireless bill to the State Farm Visa triggers the phone insurance benefit – coverage up to $600 for damage or theft. That’s an easy peace of mind perk. Just remember to pay that bill with the card every month; if you miss a month, you might lose eligibility for that period. And don’t forget to use the card at least 8 times a month if you want to keep the auto deductible reimbursement perk active – a small grocery or coffee charge each week on the card can qualify you for up to $200 back if you have an auto claim. These little habits can ensure you unlock all the extra value the card offers beyond pure cashback.

Apply through a State Farm agent for a first-year boost: According to State Farm, if you apply via a State Farm insurance agent, you could earn 5% back on insurance premiums in your first year as a special promotion. This is a temporary incentive, but if you have big insurance bills, that extra 2% bump is worth considering. Not all applicants may go through an agent, but if you’re already talking to your State Farm rep, it’s worth asking about this offer.

Redeem points strategically: Cash back from this card can be redeemed as a statement credit or bank deposit. There’s no option to funnel it directly into your insurance payments automatically, but you can manually apply your cashback to cover part of your bill. One idea: let your cashback accumulate and use it to offset your insurance premium at renewal time. For example, if you earn $100 in rewards over the year, redeem it and apply that $100 toward your next policy premium – essentially “free money” lowering your insurance cost. Since State Farm encourages using rewards for insurance, this approach aligns well with the card’s purpose.

Conclusion: Should You Get the State Farm Premier Cash Rewards Visa?

The State Farm Premier Cash Rewards Visa Signature® Card is a unique hybrid of insurance and banking – it rewards you for something you’re likely paying anyway (insurance) and throws in familiar cash-back on daily spending. For a State Farm insured, it’s a no-brainer to consider: you’re essentially getting up to $120 a year back on your premiums, plus a nice welcome bonus and useful perks like phone protection. The fact it has no annual fee means there’s little downside to holding it as a specialized tool in your wallet.

However, it’s not a powerhouse for all your spending. As we’ve detailed, its rewards on non-insurance spending are average. This card shines in a supporting role – pay your insurance with it, take the bonus cash, and use it alongside a broader 2% card or a card that covers travel/no-FTF if you need that. If you’re not with State Farm, there are plenty of other great cash-back cards to choose from that don’t require an insurance relationship.

In the end, the Premier Cash Rewards Visa makes the most sense if you check these boxes: 1) You have State Farm insurance (and plan to stick around), 2) You prefer cash back, simplicity, and no fees, and 3) You want a little extra “thank you” for your loyalty in the form of cash rebates on your premiums. If that’s you, this card can indeed be a “good neighbor” in your wallet.

Frequently Asked Questions

Who is eligible for the State Farm Premier Cash Rewards Visa?

This card is intended for current State Farm customers. You will generally need an active State Farm insurance policy or account to be approved. U.S. Bank (the card issuer) may require your State Farm policy number during application. Additionally, a good credit score (700+) is recommended for approval, since it’s a Visa Signature card. If you’re unsure about your eligibility, you can check with a State Farm agent or use U.S. Bank’s pre-qualification tools.

What is the $150 bonus on the State Farm credit card?

It’s a sign-up bonus for new cardholders. After you’re approved, if you spend $500 in purchases within the first 90 days, you will earn a $150 cash back reward. This bonus will typically post as a statement credit or rewards balance within 1–2 billing cycles after you meet the spending requirement. It’s essentially a welcome gift – $150 for $500 spend is a generous 30% return! Just be sure to meet the requirement in time.

How can I use the cash back I earn?

The cash back from this card accrues in U.S. Bank’s rewards system for State Farm cards. You can redeem your cash back as a statement credit or have it deposited into a bank account. There’s no option to directly apply it to your insurance bill through the card’s rewards portal, but redeeming to your bank account and then paying your insurance works the same. There is also no point transfer or travel redemption – this is pure cash-back, which keeps things simple. Many cardholders just take the statement credits to effectively “erase” some of their charges.

Is the State Farm Premier Cash Rewards Visa Signature worth it?

If you’re a State Farm insurance customer, it can be worth it as a complementary card. The value lies in that 3% back on insurance – basically a little loyalty dividend for staying with State Farm. Over a year, you might earn back $50, $100, or up to $120 (if you max the cap) on insurance premiums, plus rewards on gas, groceries, etc., all without an annual fee. The card also adds handy protections (cell phone insurance, etc.) that could save you money. However, for non-State Farm customers, this card isn’t accessible – and if you’re not spending much on insurance, a general cashback card might yield better overall rewards. In summary: great for State Farm devotees looking to earn a bit extra on big insurance bills; not great as a standalone everyday card for everyone else.

How does this card compare to the State Farm Good Neighbor Visa?

State Farm actually offers two personal credit cards: the Premier Cash Rewards and the Good Neighbor Visa. The Good Neighbor Visa is more of a 0% APR/low-rate card – it doesn’t focus on cash-back rewards. It offers 0% intro APR for 18 months on purchases and balance transfers, but it doesn’t earn 3% on anything. Think of Good Neighbor Visa as an option if you need to finance a purchase or pay off debt with no interest for a while, whereas the Premier Cash Rewards is for earning cash back. Both have no annual fee, and both are only for State Farm customers. Depending on your needs, you choose cash back vs. low APR. Some State Farm customers actually carry both – one for the 0% period, and the other for ongoing rewards once they’re ready to pay in full each month.

Supercharge Your Credit Cards

Experience smarter spending with Kudos and unlock more from your credit cards. Earn $20.00 when you sign up for Kudos with "GET20" and make an eligible Kudos Boost purchase.

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)

.webp)

.webp)

.jpg)